Ideally, a building makes life pleasantly unremarkable for both its occupants and its owners: It provides physical shelter that keeps the indoor climate comfortable and delivers consistent monetary returns. But these predictable outcomes require a great deal of investment and—crucially—depend on the performance and reliability of surrounding systems that are largely invisible to most people.

The physical and financial foundation of every building is a large set of assumptions that rarely receive much scrutiny. Perhaps the most powerful assumption is that the local climate outdoors will remain stable.

If you live, work, or invest in a building, it’s important to understand its surrounding systems and the risks they face as a warmer atmosphere changes local climates.

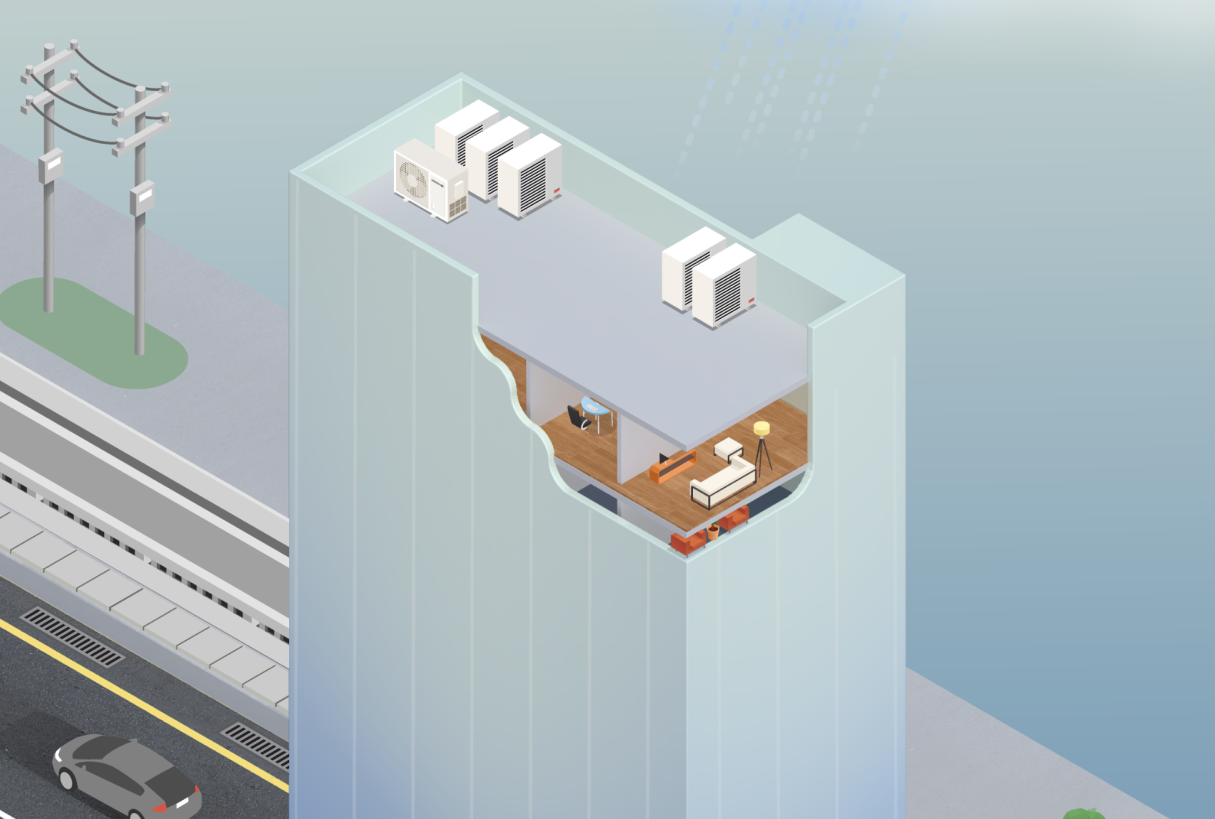

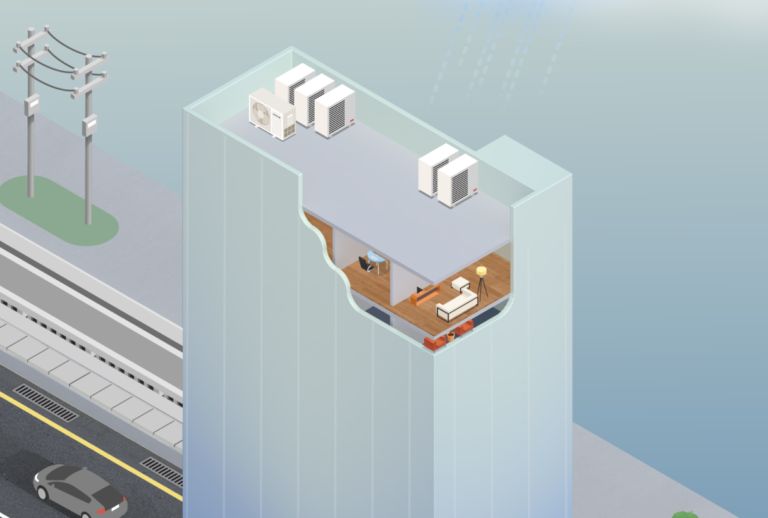

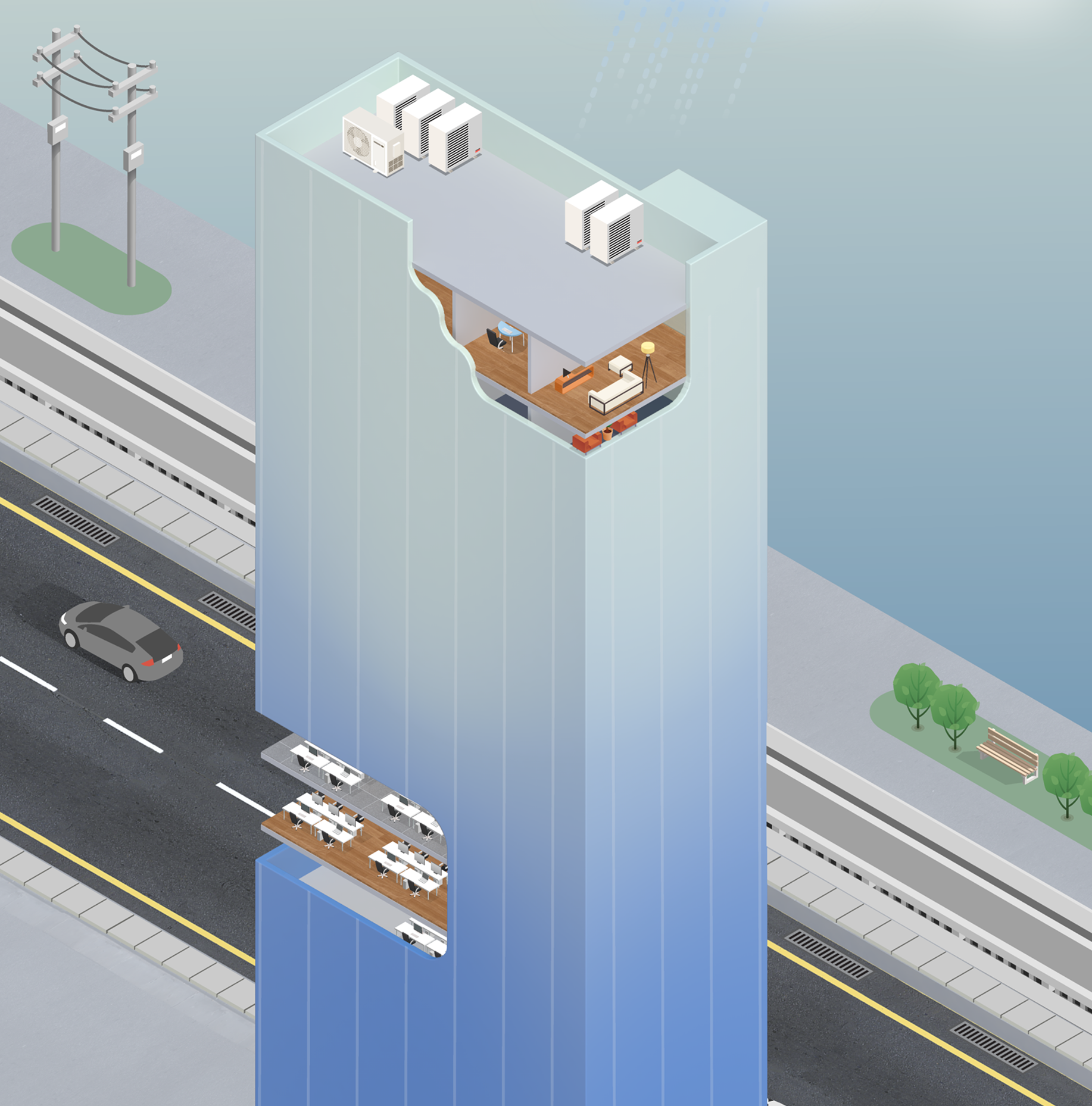

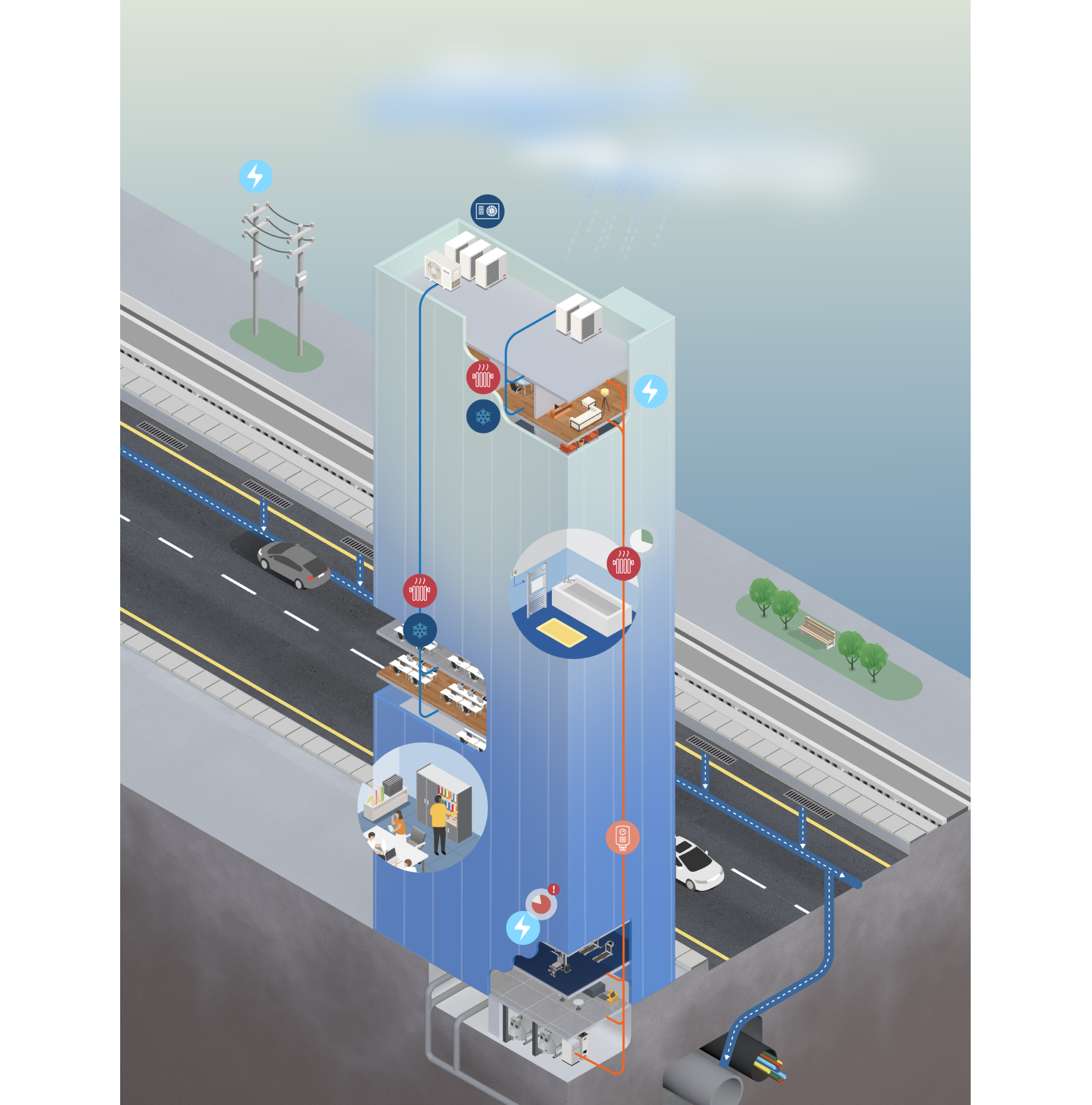

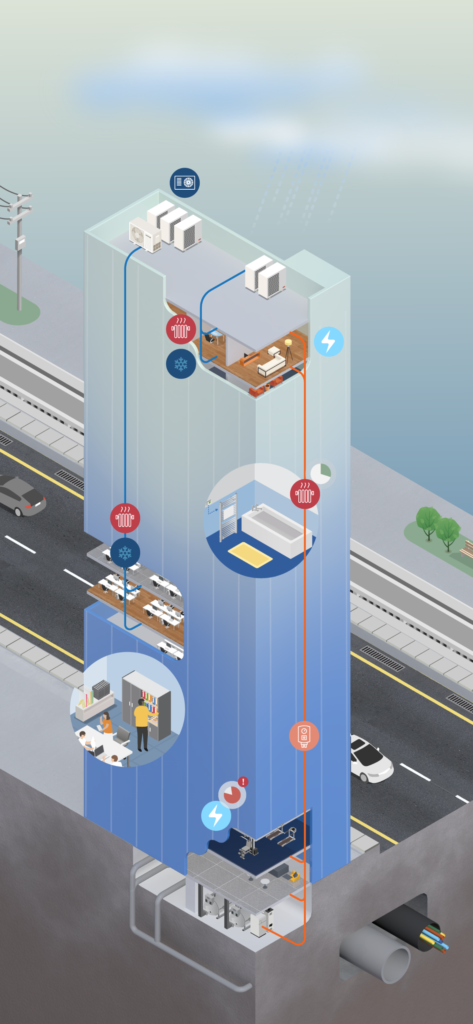

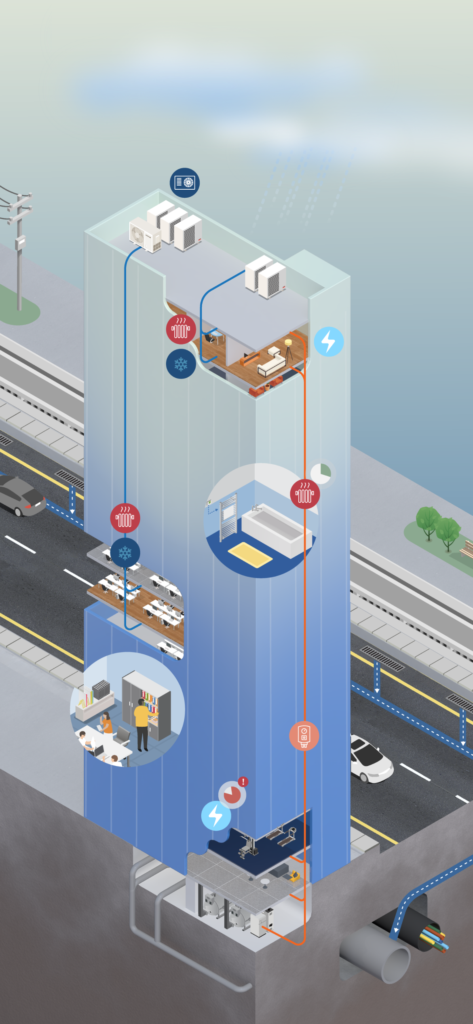

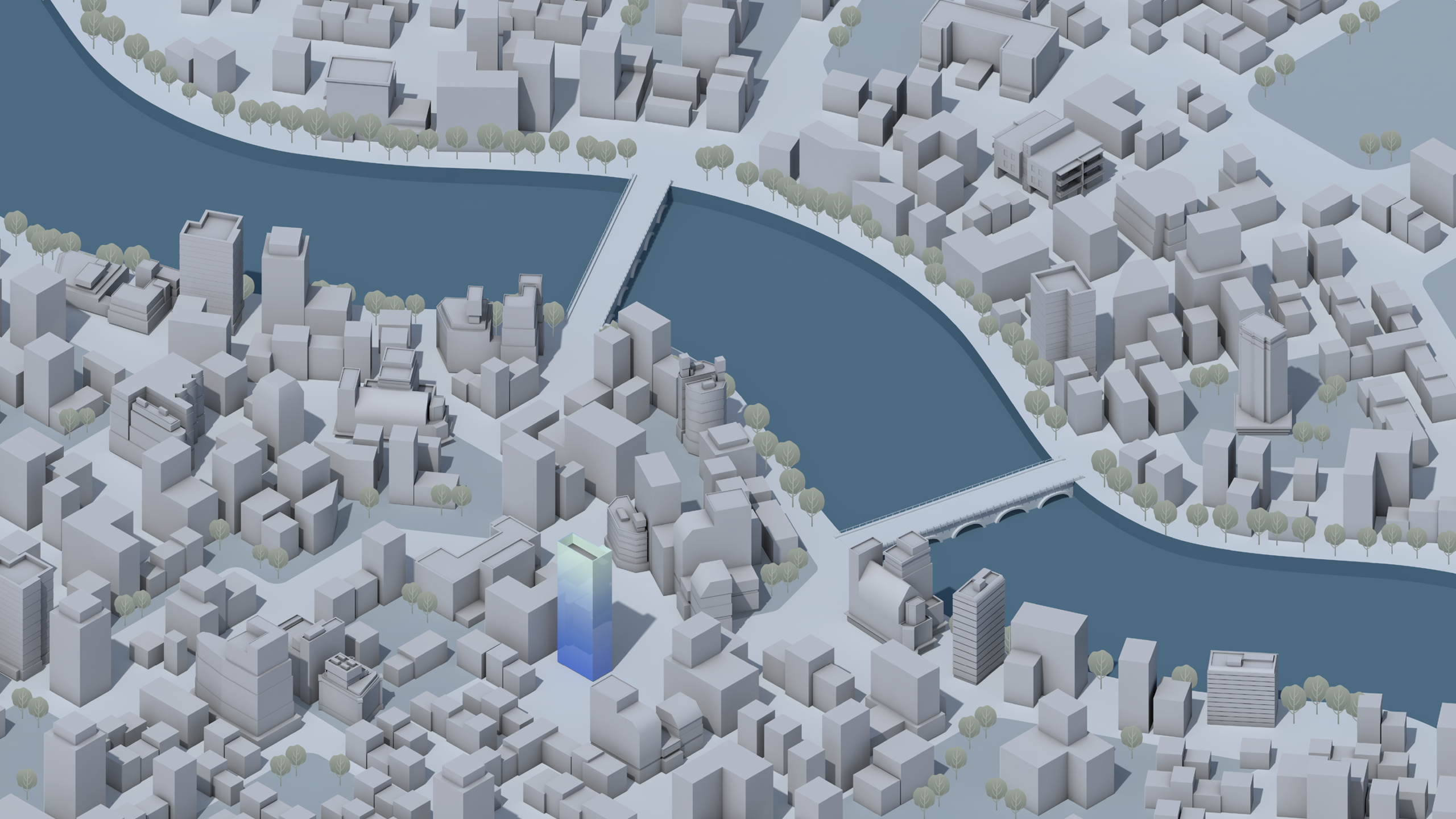

Let’s examine a 15-story building with interior spaces that are a mix of office, residential, and retail. The resulting observations and insights can be applied to any building type (e.g., apartment, hospital, shopping mall, industrial warehouse, or data center). We will pay special attention to the heating, ventilation, and air conditioning (HVAC) systems.

The occupants want comfort, cleanliness, and functionality inside, no matter what is going on outside. To deliver this, the building owner makes assumptions about the local climate (e.g., temperature ranges, precipitation amounts, wind speeds, etc.) and weighs the expense of stronger, more insulating materials and higher-quality, more robust and powerful equipment against cost concerns.

Construction companies and other contractors follow building codes, engineering standards, and other norms. All of these guidelines are based on past ranges of temperature, rainfall, and wind speed. Implicitly, they assumed that those past patterns would persist and that the risks of flooding and wildfire were stable, well-known, and low or nonexistent.

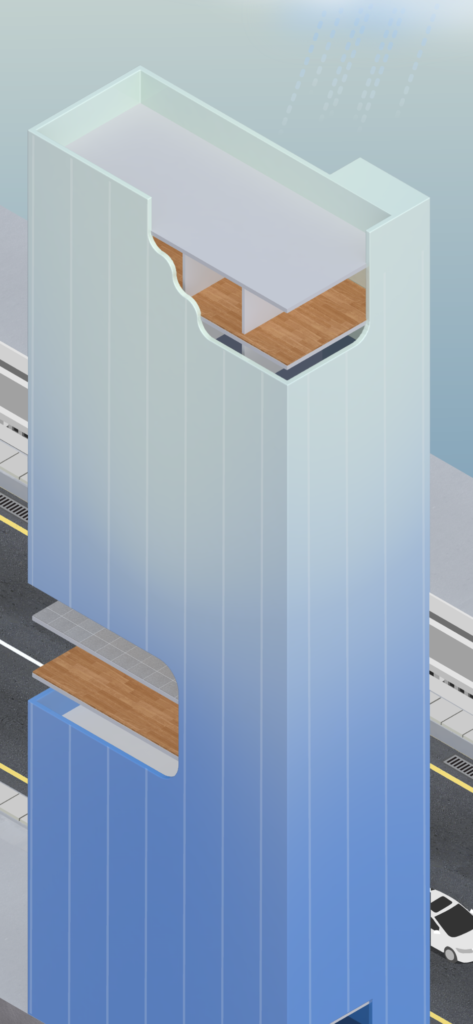

This building is clad in glass, and its windows do not open. The quality of the glass and the way it was installed affect how much light it lets in and the interior temperature.

A glass building without openable windows is like a greenhouse: Light and heat can penetrate the windows, but air cannot get out. When the sun is shining, it can get very warm inside, even if the outdoor temperature is mild. A glass building like this will often need to run air conditioning when temperatures are above 50 to 60°F (10 to 15°C). Glass does not insulate well, so at night (or in winter) when the weather cools, this building’s heating system must get to work.

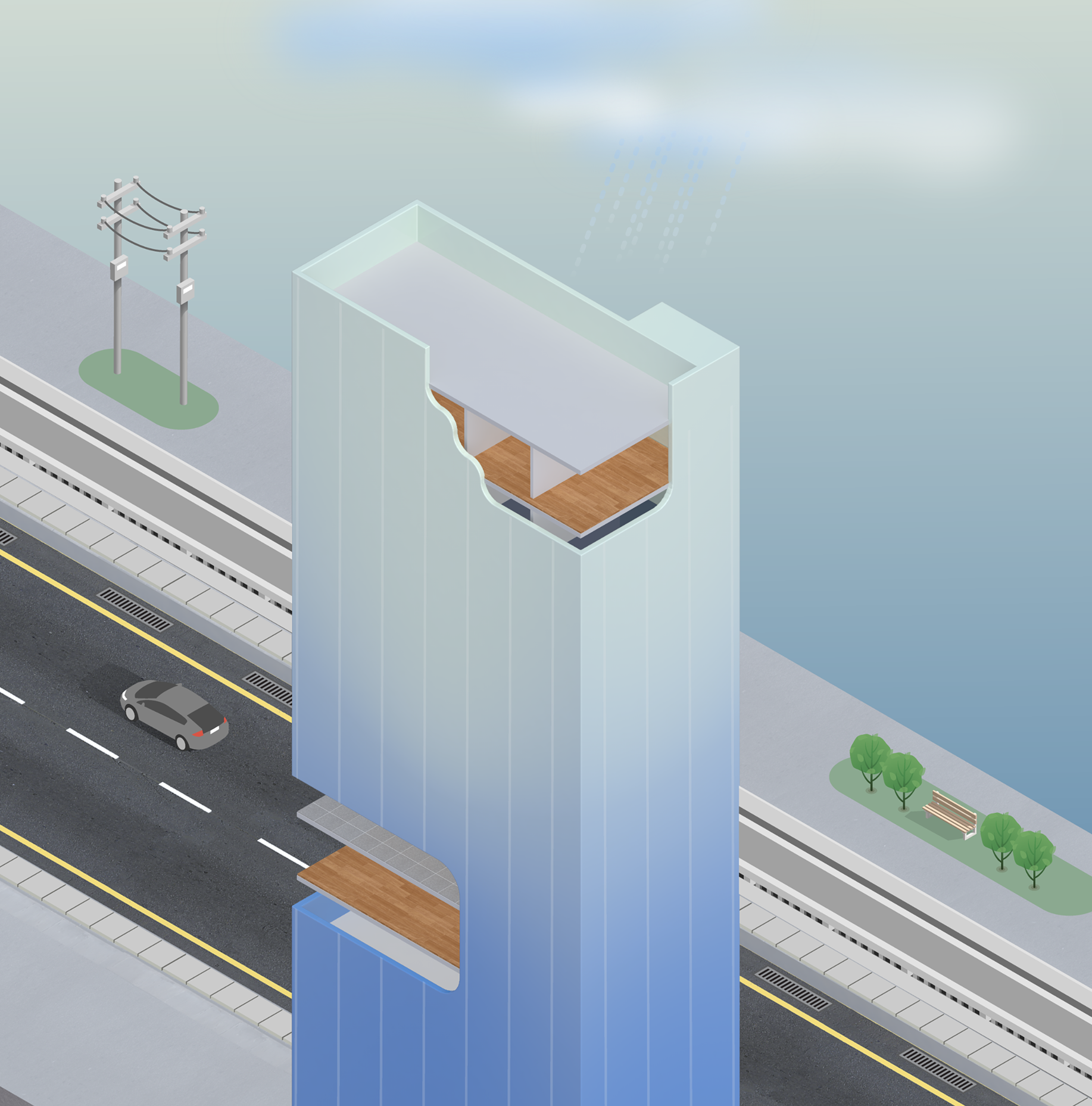

HVAC systems require a large amount of space, and builders have to decide where to put them. The basement and roof are attractive locations because they cannot be rented out, but each poses a risk. The basement may be vulnerable to flooding, while the roof is exposed to wind, precipitation, and the full range of outdoor temperatures, which may influence both HVAC performance and longevity.

The building’s HVAC system is part of the broader energy and air systems that also have limits. Temperatures outside the expected range can strain or break the power system. Wildfire smoke, even drifting from far away, can make indoor air toxic. Building owners may need to invest in equipment such as backup batteries, generators, and air filtration systems to maintain indoor conditions.

Water, sewer, communications, transportation, and other systems also have to function as planned. Rainfall amounts beyond what the storm sewers were designed to handle can flood the garage, lobby, and train stations. Rising seas can contaminate aquifers with saltwater. Extreme heat can make sidewalks too hot for pedestrians and ruin asphalt roads and airport tarmacs.

As local weather patterns shift further from their past stable ranges, these systems will struggle to deliver the same level of comfort and control for the people inside and financial predictability for the building’s owners. Do the owners see these new risks? Do they see the building at all? Who takes responsibility for this increasingly vulnerable asset?

Let’s examine a 15-story building with interior spaces that are a mix of office, residential, and retail. The resulting observations and insights can be applied to any building type (e.g., apartment, hospital, shopping mall, industrial warehouse, or data center). We will pay special attention to the heating, ventilation, and air conditioning (HVAC) systems.

The occupants want comfort, cleanliness, and functionality inside, no matter what is going on outside. To deliver this, the building owner makes assumptions about the local climate (e.g., temperature ranges, precipitation amounts, wind speeds, etc.) and weighs the expense of stronger, more insulating materials and higher-quality, more robust and powerful equipment against cost concerns.

Construction companies and other contractors follow building codes, engineering standards, and other norms. All of these guidelines are based on past ranges of temperature, rainfall, and wind speed. Implicitly, they assumed that those past patterns would persist and that the risks of flooding and wildfire were stable, well-known, and low or nonexistent.

This building is clad in glass, and its windows do not open. The quality of the glass and the way it was installed affect how much light it lets in and the interior temperature.

A glass building without openable windows is like a greenhouse: Light and heat can penetrate the windows, but air cannot get out. When the sun is shining, it can get very warm inside, even if the outdoor temperature is mild. A glass building like this will often need to run air conditioning when temperatures are above 50 to 60°F (10 to 15°C). Glass does not insulate well, so at night (or in winter) when the weather cools, this building’s heating system must get to work.

HVAC systems require a large amount of space, and builders have to decide where to put them. The basement and roof are attractive locations because they cannot be rented out, but each poses a risk. The basement may be vulnerable to flooding, while the roof is exposed to wind, precipitation, and the full range of outdoor temperatures, which may influence both HVAC performance and longevity.

The building’s HVAC system is part of the broader energy and air systems that also have limits. Temperatures outside the expected range can strain or break the power system. Wildfire smoke, even drifting from far away, can make indoor air toxic. Building owners may need to invest in equipment such as backup batteries, generators, and air filtration systems to maintain indoor conditions.

Water, sewer, communications, transportation, and other systems also have to function as planned. Rainfall amounts beyond what the storm sewers were designed to handle can flood the garage, lobby, and train stations. Rising seas can contaminate aquifers with saltwater. Extreme heat can make sidewalks too hot for pedestrians and ruin asphalt roads and airport tarmacs.

As local weather patterns shift further from their past stable ranges, these systems will struggle to deliver the same level of comfort and control for the people inside and financial predictability for the building’s owners. Do the owners see these new risks? Do they see the building at all? Who takes responsibility for this increasingly vulnerable asset?

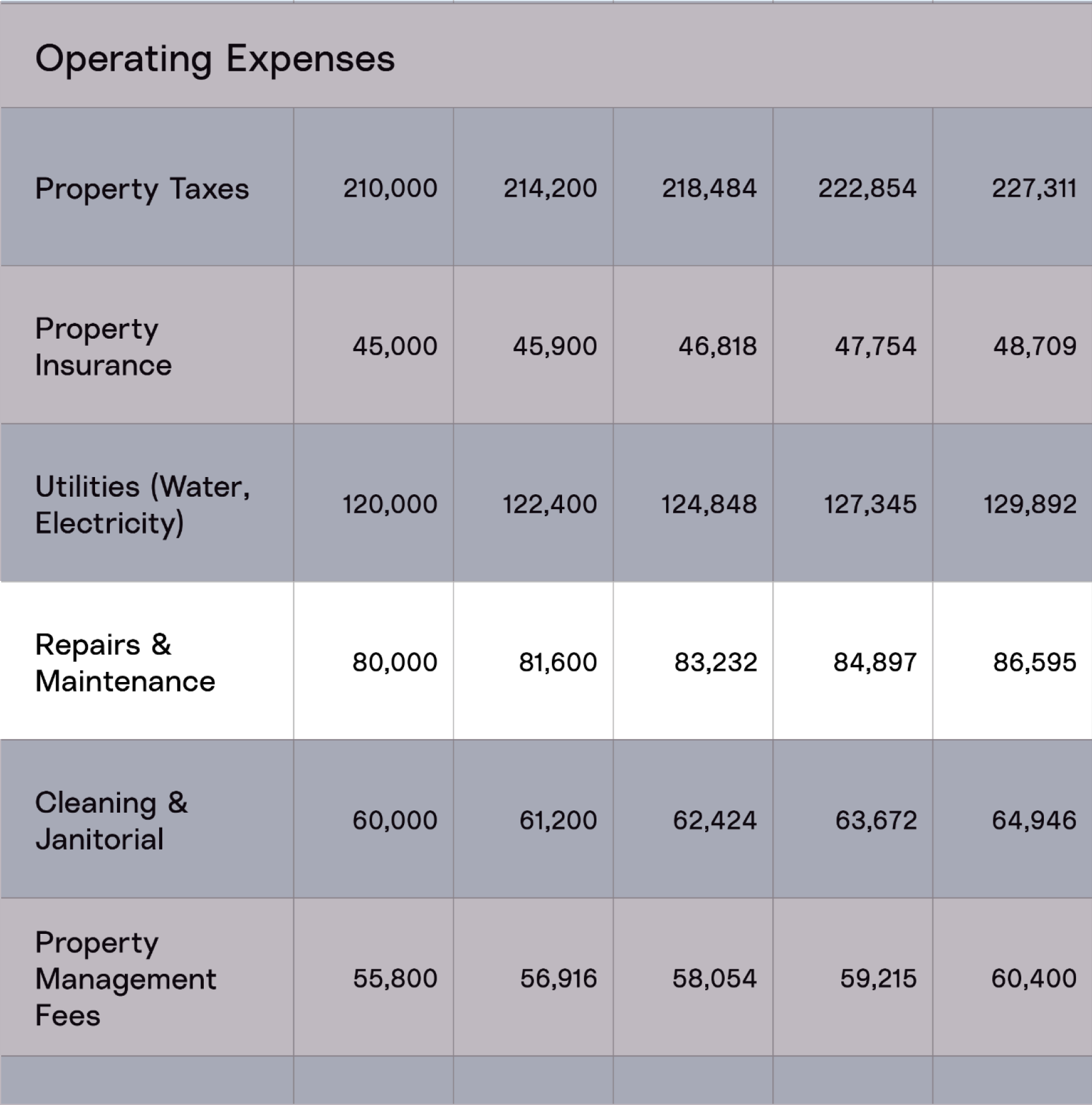

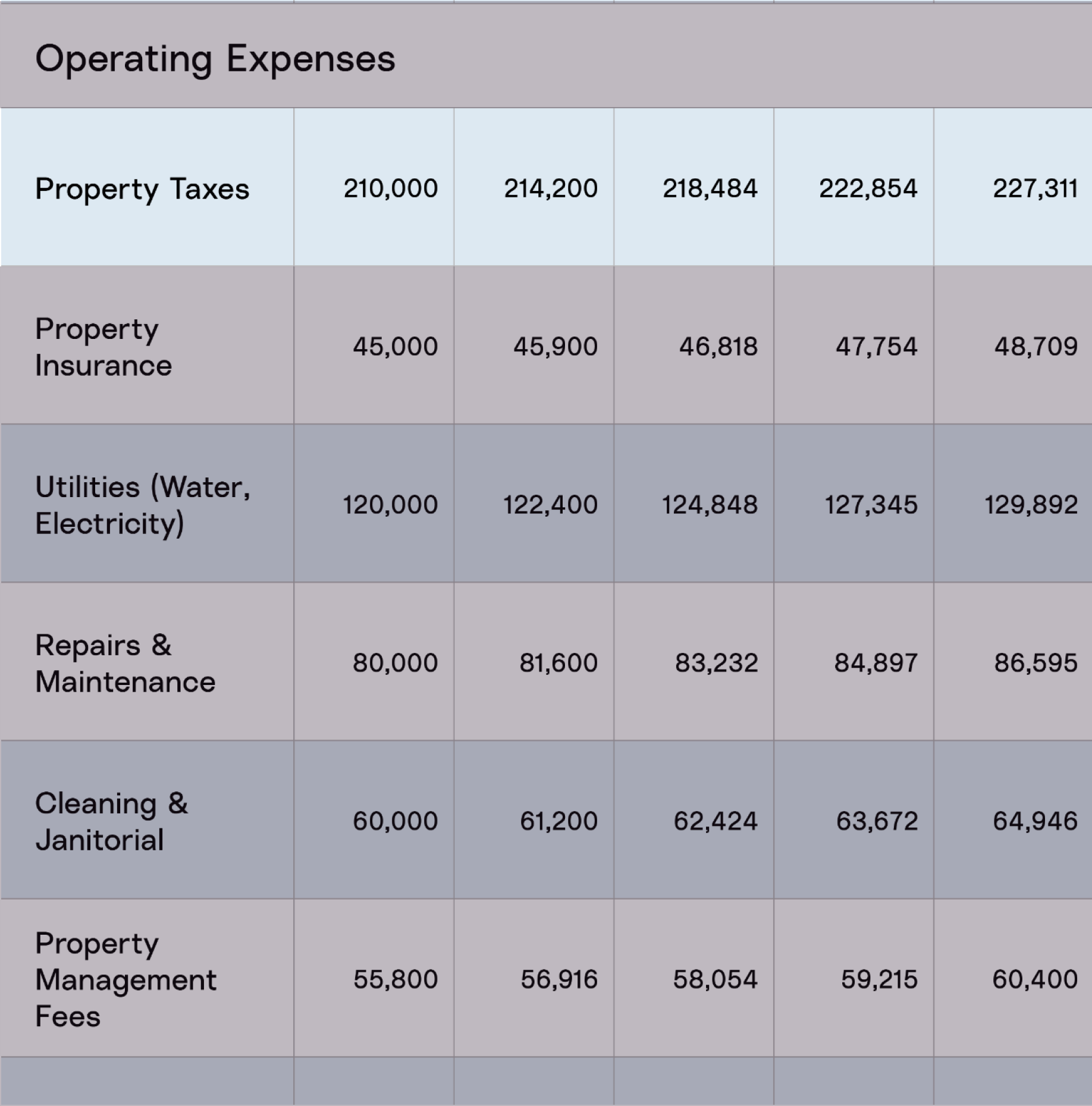

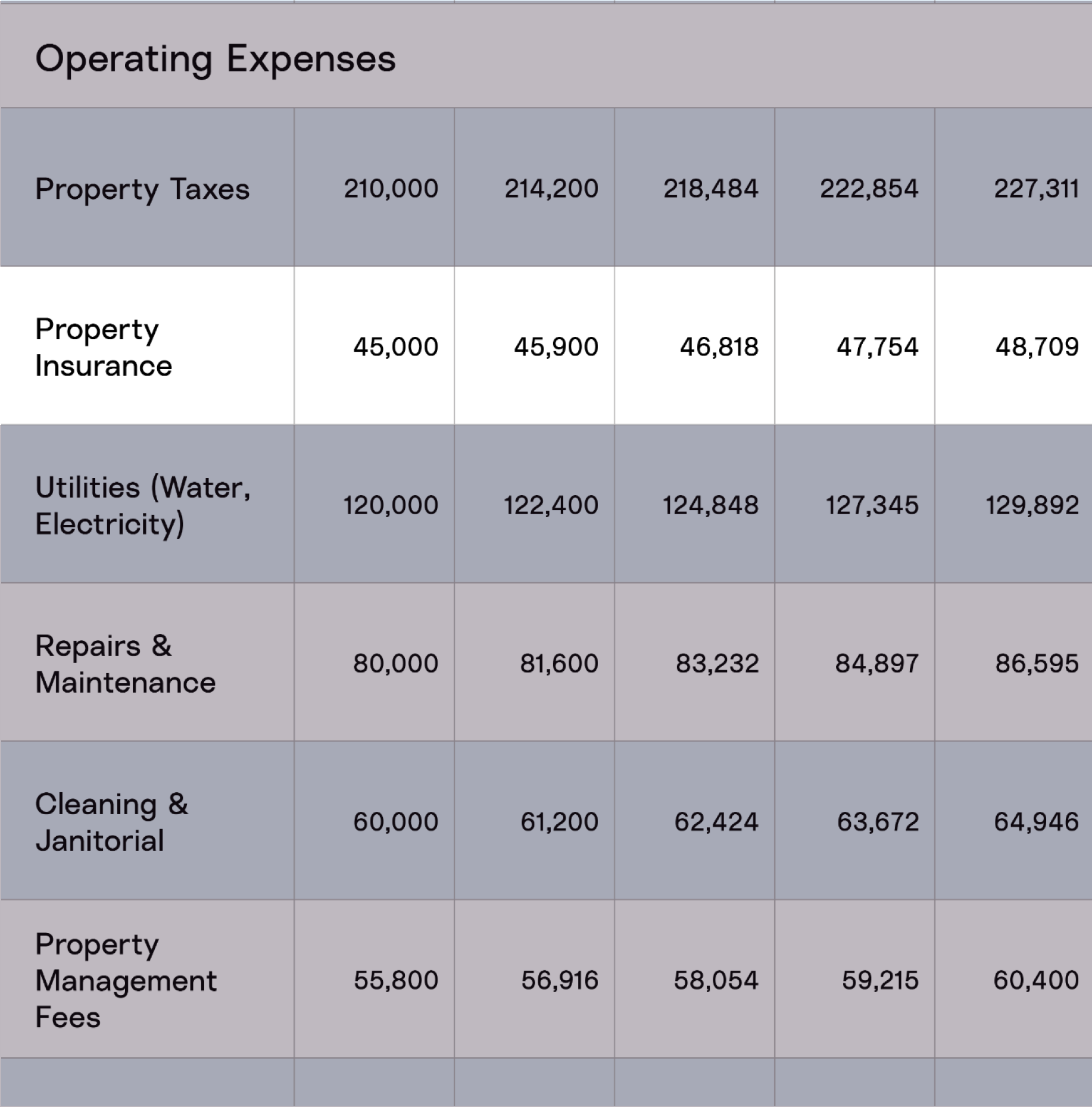

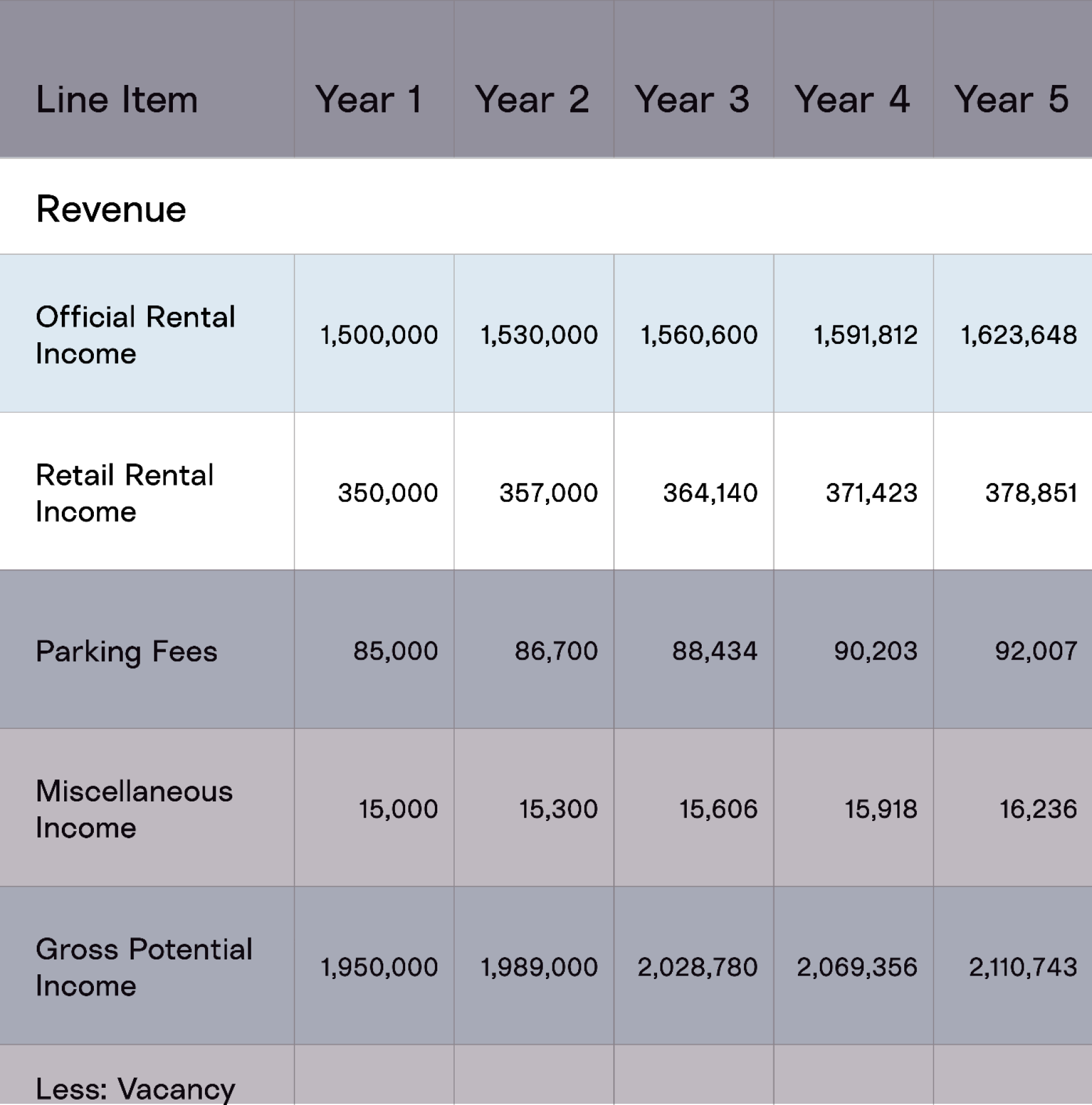

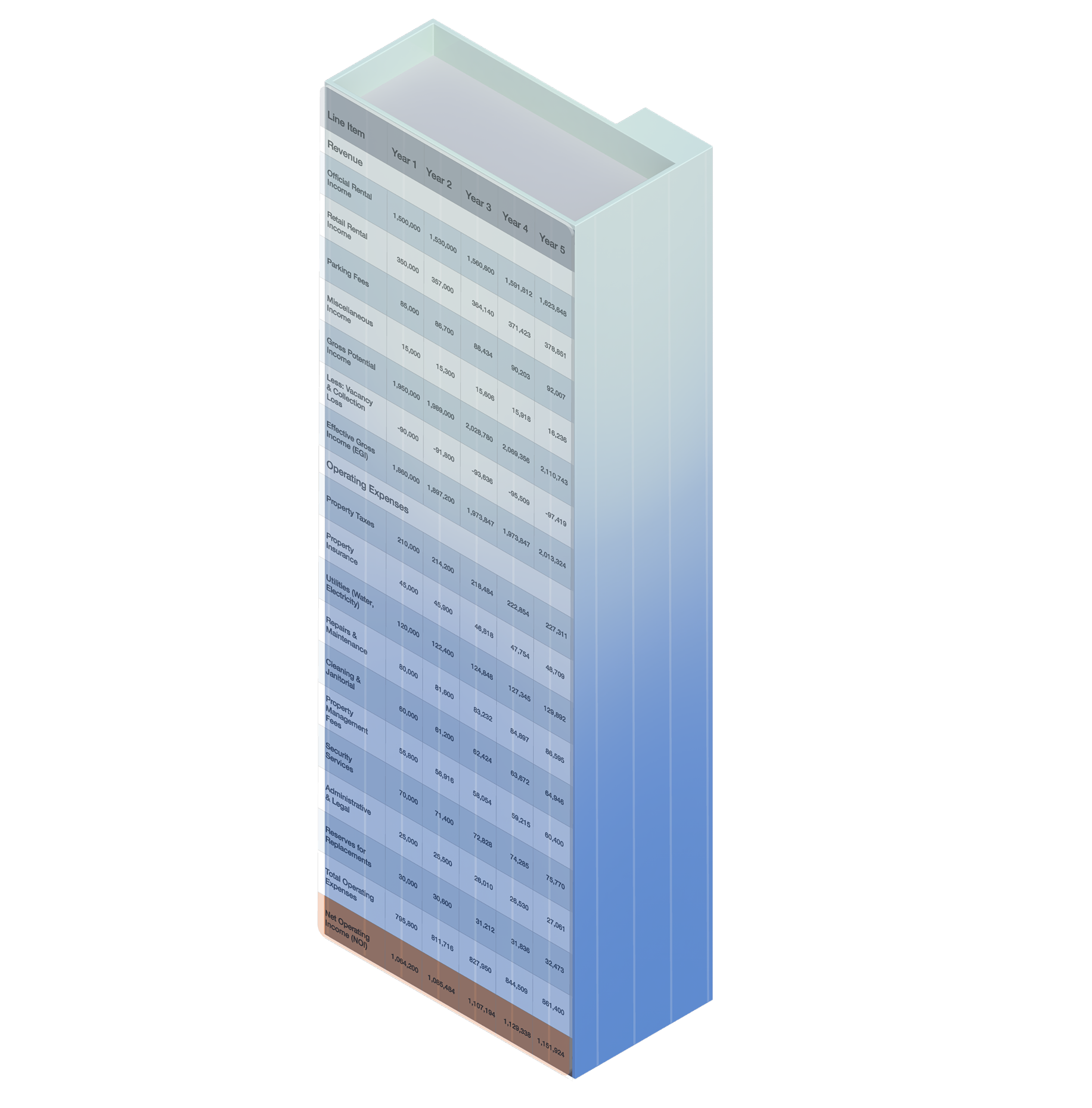

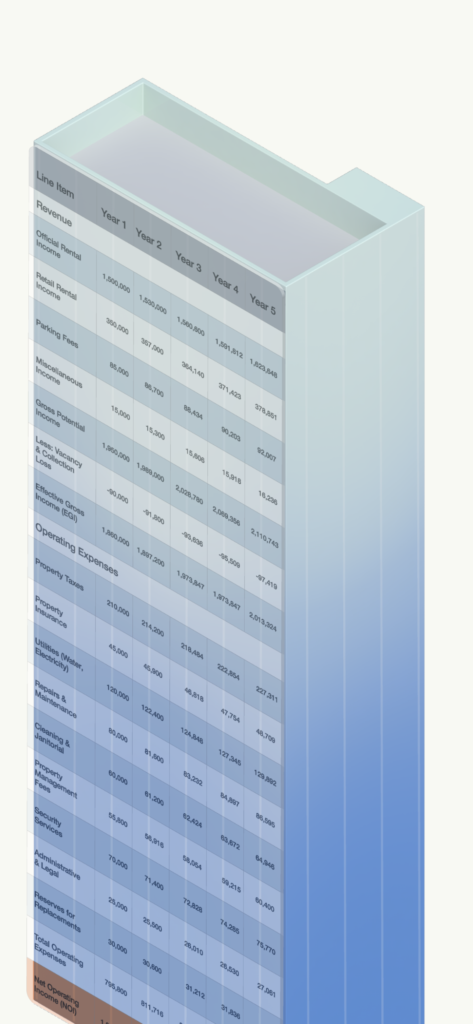

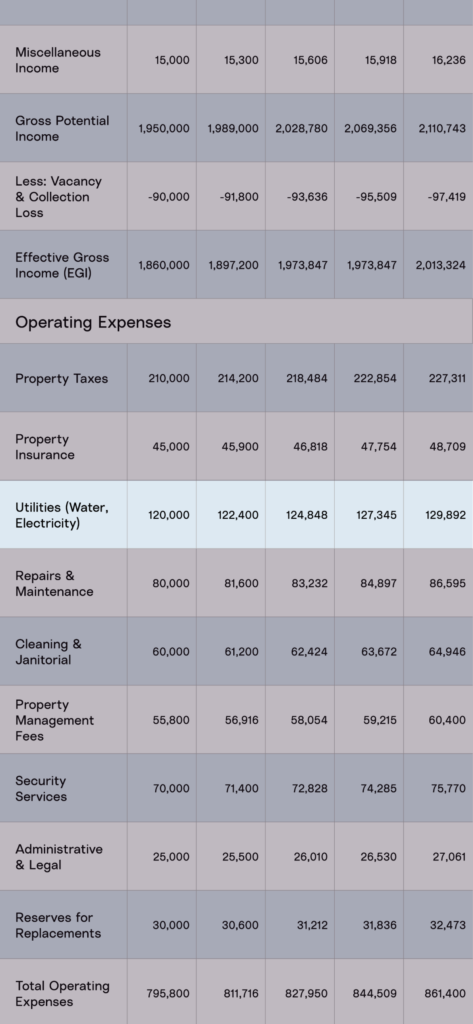

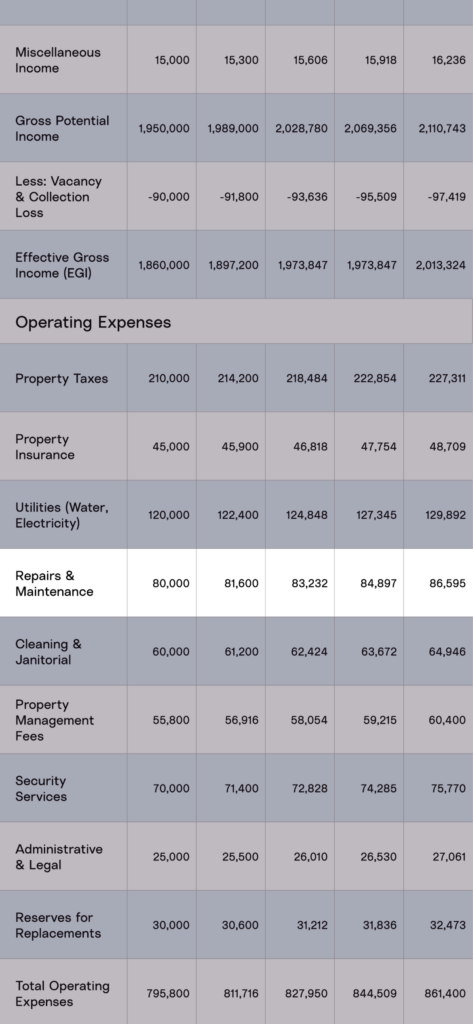

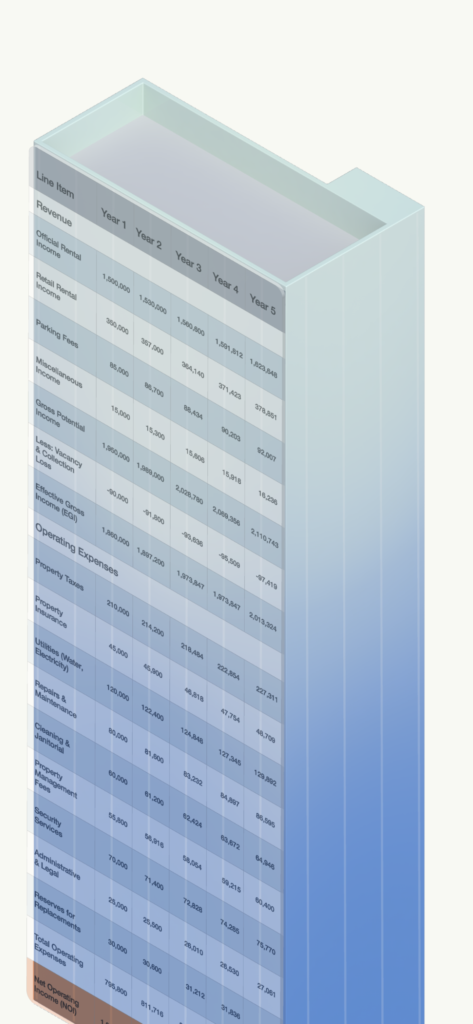

Buildings have a parallel existence in the world of finance. Unlike the physical world with its three dimensions, the financial representation of a building is two-dimensional. The alchemy of accounting transforms materials and systems into numbers on a spreadsheet. Examining that spreadsheet and the assumptions embedded in it offers insight into the global financial system and its vulnerability to climate change.

Viewed through the eyes of an investor, the building is simplified, compressed into the key financial variables. The three-dimensional building is literally flattened as the physical characteristics disappear into rows and columns of numbers.

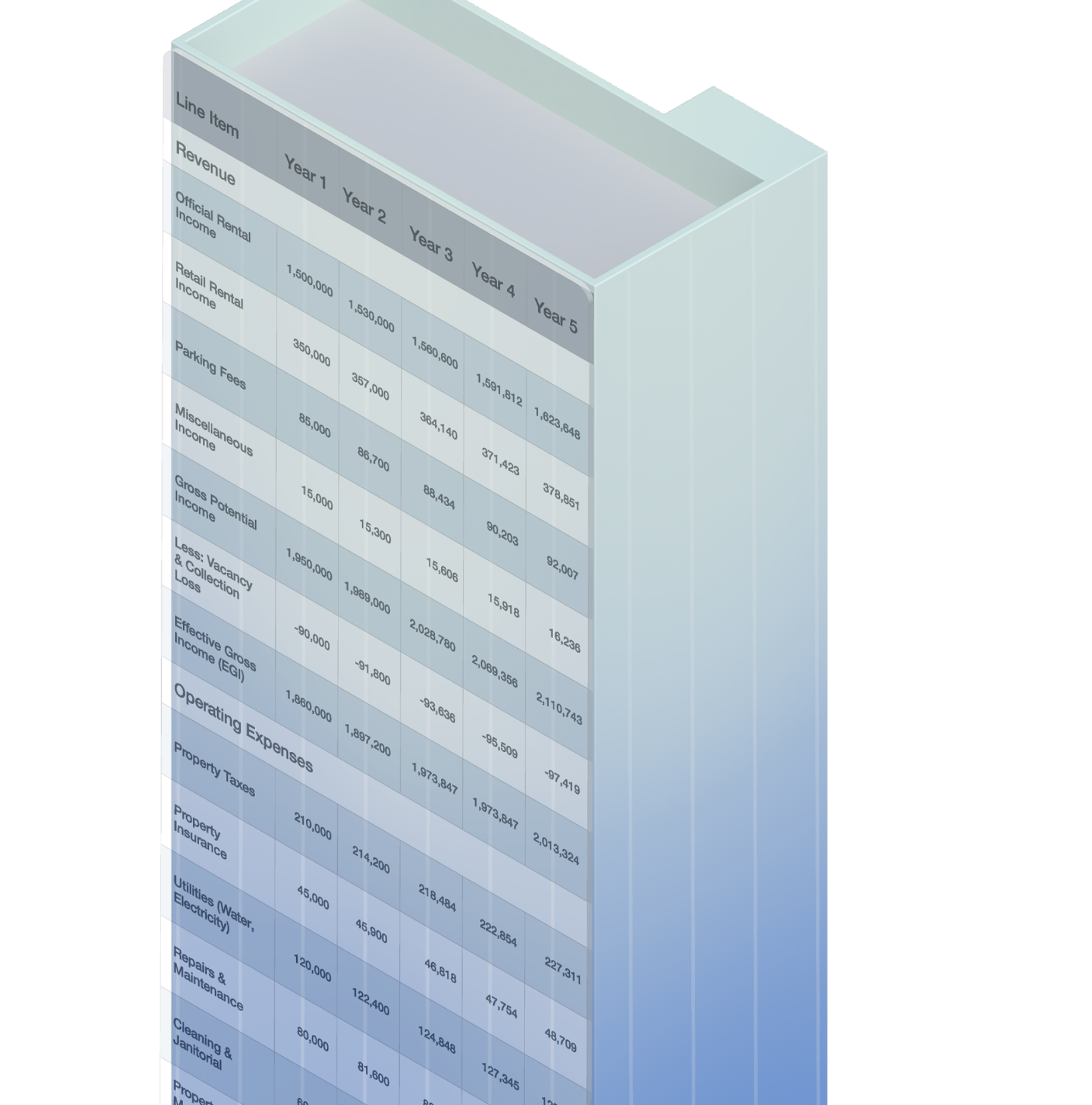

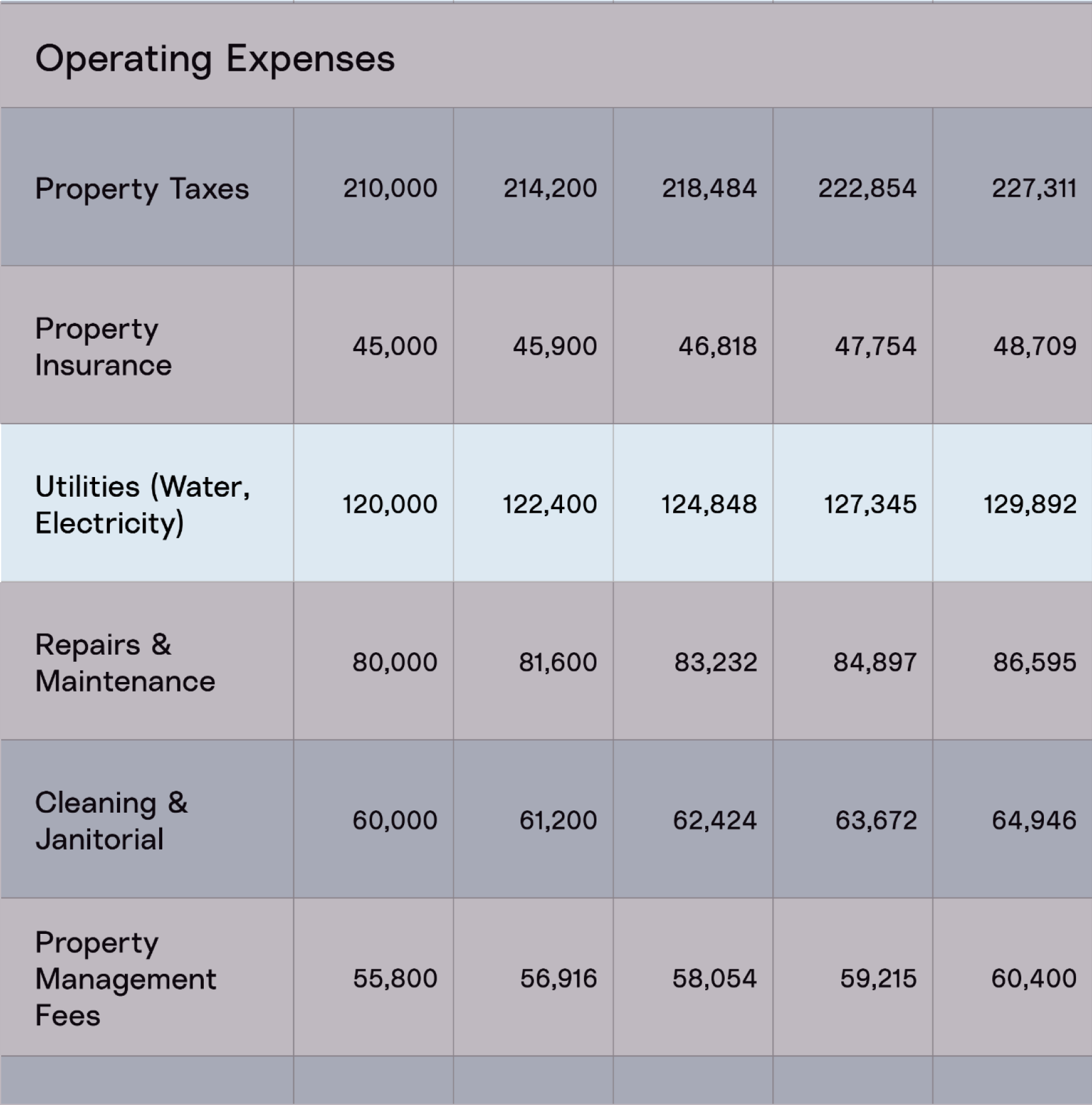

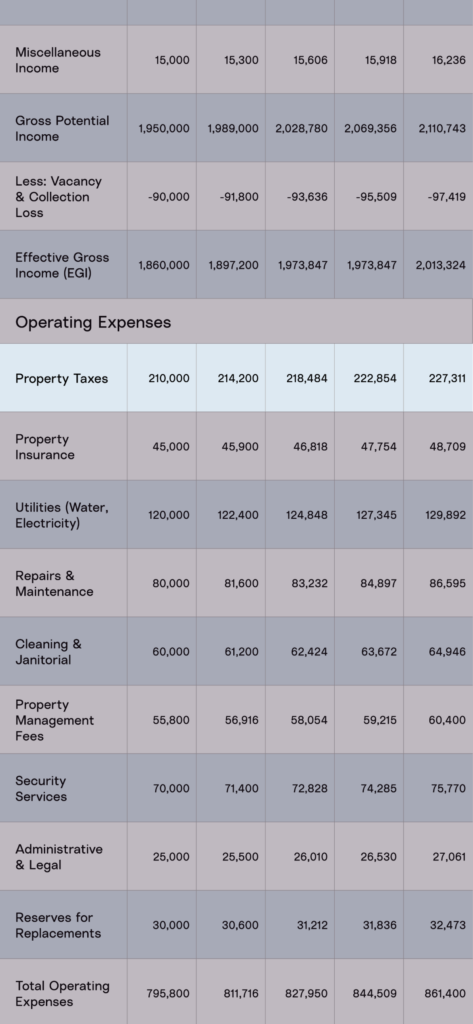

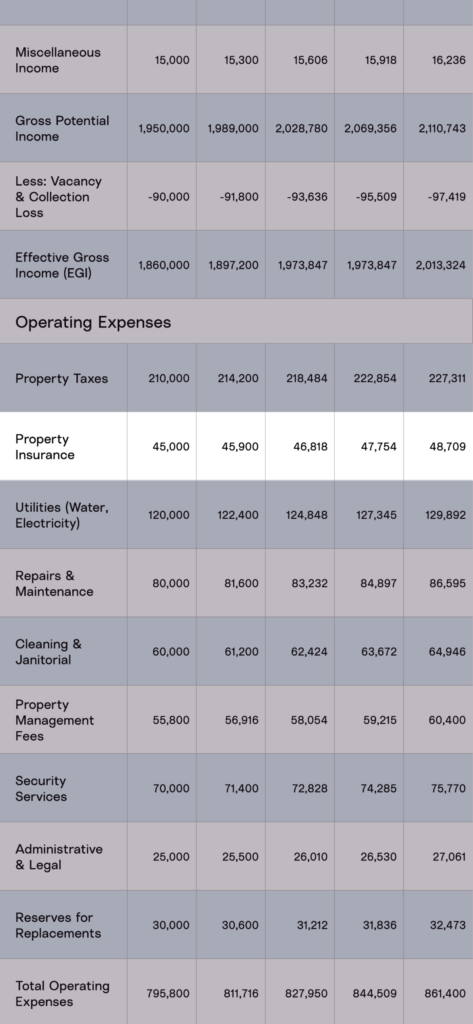

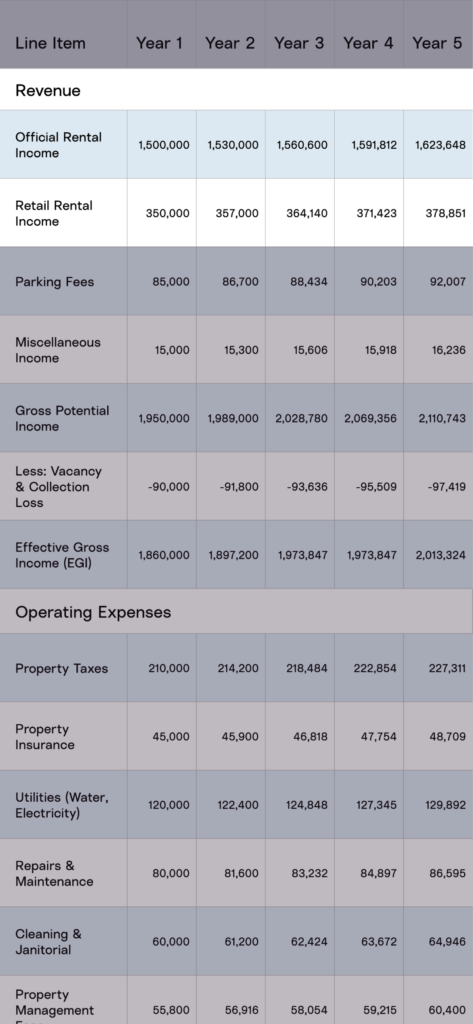

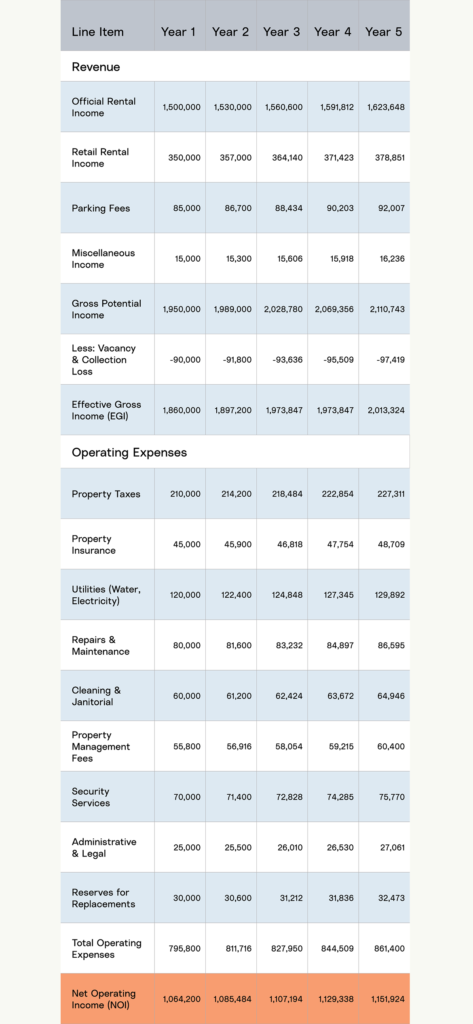

Spreadsheets are the common language of finance. Investment in a building can be summarized into money in (revenue), money out (expenses), and money invested (initial cost). Income statements for businesses and buildings look basically the same. Future years are all based on Year 1, with some assumed steady, incremental annual adjustment based on historical trends, which is copied and pasted to fill out the cells that project the future of the owner’s investment.

How different is the outside temperature from the desired indoor temperature? And how much does it cost to maintain the indoor climate?

Do you need to repair or upgrade your heating or cooling? Will tenants demand air filters?

Will the city have to invest in expensive forms of climate adaptation?

Extreme weather events are becoming more frequent, more costly, and harder to predict. Business interruption will drive down revenue. Insurance coverage will become more expensive and less available, raising costs.

Will demand for living and working in this neighborhood, city, or region change as it becomes hotter, wetter, or more expensive?

The spreadsheet presents one simplified, smooth future, devoid of variability or shocks. Yet when building a portfolio and considering many potential investments, many investors will barely consider even the few details that are in the rows and columns. They will further synthesize the spreadsheet into a single number, such as return on investment (ROI). This extreme reduction in complexity makes it easier to compare buildings of different ages, materials, and qualities in different places.

Historically, a building might have been paid for by a single investor, perhaps with a loan from a local bank. In recent decades, dividing ownership into standardized units has increased the amount of capital available, but “ownership” has become less clear as multiple investors often share the financing of new and existing buildings. Who is responsible for a building with many, often temporary, owners?

Owners typically augment their equity with debt. Here we show a simple structure, with junior and senior debt. Participants in those layers, whether buying bonds or making loans, receive a defined interest rate and bear less risk than equity holders. A building could have dozens of investors across the equity and debt layers, and each of these investments is only part of each investor’s portfolio.

To an investor in a real estate fund, a building is often reduced to a single value in a spreadsheet: an estimated return based on one smooth forecast. All physical details and uncertainties have been flattened. Investors often have little awareness of the physical risks of buildings they own or the decisions that may be required to mitigate increasing risks in a changing climate.

Viewed through the eyes of an investor, the building is simplified, compressed into the key financial variables. The three-dimensional building is literally flattened as the physical characteristics disappear into rows and columns of numbers.

Spreadsheets are the common language of finance. Investment in a building can be summarized into money in (revenue), money out (expenses), and money invested (initial cost). Income statements for businesses and buildings look basically the same. Future years are all based on Year 1, with some assumed steady, incremental annual adjustment based on historical trends, which is copied and pasted to fill out the cells that project the future of the owner’s investment.

How different is the outside temperature from the desired indoor temperature? And how much does it cost to maintain the indoor climate?

Do you need to repair or upgrade your heating or cooling? Will tenants demand air filters?

Will the city have to invest in expensive forms of climate adaptation?

Extreme weather events are becoming more frequent, more costly, and harder to predict. Business interruption will drive down revenue. Insurance coverage will become more expensive and less available, raising costs.

Will demand for living and working in this neighborhood, city, or region change as it becomes hotter, wetter, or more expensive?

The spreadsheet presents one simplified, smooth future, devoid of variability or shocks. Yet when building a portfolio and considering many potential investments, many investors will barely consider even the few details that are in the rows and columns. They will further synthesize the spreadsheet into a single number, such as return on investment (ROI). This extreme reduction in complexity makes it easier to compare buildings of different ages, materials, and qualities in different places.

Historically, a building might have been paid for by a single investor, perhaps with a loan from a local bank. In recent decades, dividing ownership into standardized units has increased the amount of capital available, but “ownership” has become less clear as multiple investors often share the financing of new and existing buildings. Who is responsible for a building with many, often temporary, owners?

Owners typically augment their equity with debt. Here we show a simple structure, with junior and senior debt. Participants in those layers, whether buying bonds or making loans, receive a defined interest rate and bear less risk than equity holders. A building could have dozens of investors across the equity and debt layers, and each of these investments is only part of each investor’s portfolio.

To an investor in a real estate fund, a building is often reduced to a single value in a spreadsheet: an estimated return based on one smooth forecast. All physical details and uncertainties have been flattened. Investors often have little awareness of the physical risks of buildings they own or the decisions that may be required to mitigate increasing risks in a changing climate.

In the physical world, buildings are complex, sheltering and serving specific people in specific places under specific conditions; in financial markets, buildings are simple, producing income and wealth on spreadsheets and in accounts. We speak to many audiences who assume that sophisticated capital markets—banks, investment managers, insurance companies, etc.—incorporate all relevant factors into their pricing, including the changing climate, as a matter of course. The reality is the opposite: The sophistication and scale of global capital markets have encouraged increased standardization and abstraction.

In a stable climate, the gap between the local, concrete reality of stone, steel, and glass and the placeless, symbolic representations of money was bridged by assumptions that the future would be like the past. Investors didn’t need to think in terms of topography, materials, or forces of nature. Capital flowed around the world without much attention to the physical world. In a climate that is no longer stable, such assumptions become dangerous oversimplifications.

Risks posed by a changing climate require a third perspective. Zooming out, we are reminded that every building, every piece of infrastructure, and every system is part of a community and broader society. Buildings are perhaps the most obvious intersection of a changing climate and human civilization, but all of our institutions and cultures—from utilities to businesses to governments to civic traditions—also assume that the climate of the future will be just like the climate of the past. As a result, new risks are not only all around us but also connected.

Your home, your business, your building, and your investments share in and contribute to the risks of your community. The best way to address this is to start with a foundation of climate literacy, and to integrate that literacy into investment and banking, property management, architecture and engineering, city planning, city governance, and civic culture. The more everyone can see the world through this new lens, the more we can all prepare, adapt, and prosper.

Illustrations by Jing Zhang