Every day, after some amount of sleep, each of us wakes up and starts being bombarded by new content. A few of the appeals for our attention offer straightforward information, but most are packaged as something greater: an explanation, a strategy, or even a truth. Influencers, appealing to our innate yearning for sensemaking and our (and their) desire to be seen favorably by others, not only claim to have discovered patterns or schemes that govern the noisy world, but promise us useful, profitable shortcuts that other people don’t yet see.

This daily barrage of grand narratives and science-y life hacks is exciting and distorting. We want it, but sense that it’s not good for us. It affects how we see the world, our relationships with other people, and our sense of who we are. Somehow, the abundance makes us hungry for even more new ideas. It makes us curious if perhaps the hard problems, the ones that we know we should work on, might be solved by something as simple as a transaction.

Our insatiable hunger for quick hits of content may be new to society at large, but it’s been a characteristic of the investment business since its inception. Financial markets are information processing systems, so they attract curious people. But the word “curious” can have different meanings. The English word derives from the Latin root cura (care). Over time, the word grew to mean a strong desire to know and understand. In Chinese, however, the word is hàoqí, which translates to “good strange.” And in German, the word is neugierig, which translates to “new greedy,” or greedy for new things.

Working in the investment business, I came to see that more than caring or wanting to really understand, more than just being interested in the novel and strange, investors are often simply greedy for new ideas, themes, models, and trades. And now the rest of the world is becoming neugierig. It’s not good.

Neugierig

I spent nearly two decades at a global investment firm. I was hired partly because I was an outsider to the industry (e.g., I had never read The Wall Street Journal and didn’t know that “bonds” and “fixed income” referred to the same thing) after credulous insiders had led the firm astray in the Asian Financial Crisis. I was hopeful that I could have a couple of good ideas that would help out. More than one good idea a year felt like it would be a stretch.

But then I started going to what the firm called The Morning Meeting. There, in an amphitheater-styled room, analysts pitched new ideas to an audience of 200 or so investors in suits, who then interrogated them. Typically, about five analysts offered a buy or sell recommendation each day. At first, five ideas in 30 minutes felt exciting. But markets are closed only on weekends and major holidays, so that adds up to more than 1,000 arguments each year that a particular stock, bond, commodity, currency, etc., is misunderstood and mispriced, all before 9 a.m.

I was curious: How could people hang onto the truth if they were relentlessly asked to reconsider it? And what kind of relationship would these people have with the world if their livelihood depended on being smarter than everyone else? Would they be comfortable with enduring, frustratingly well-understood truths, or would they constantly be looking for clever angles?

After some early success at the firm, I was asked to oversee economic research. There was a young Austrian man in our department named Julius who had worked at the European Central Bank, had a PhD from a Spanish university, and had grown up on a farm in his home country. (“My parents grow subsidies,” he once told me.) I arranged for him to sit with bond investors, observe their behavior, and see if he could help improve their performance.

A couple of months later, he told me he had found something. The gist was that the best information about the state of the economy came out quarterly, and that if a portfolio manager, instead of trying to beat the market every hour of every day, simply waited until new quarterly data came out and then reacted by following a simple buy/hold/sell rule that Julius had devised, performance would improve because the trades would consistently be more right than wrong and because the clients wouldn’t lose money from trading costs. It was clever and elegant. I wasn’t technically skilled enough to tell if the modeling was perfectly sound, and no one could know if it would work as Julius theorized, but it was clearly worth sharing his idea with a group of bond managers. We convened a meeting to talk about the research. We wound up in a much more interesting conversation.

Julius explained his approach, shared the statistical evidence for low-frequency information, showed the backtesting he had done, and projected performance of a model portfolio under different scenarios. I expected questions, but the first reaction from the bond managers was a declaration: “We can’t use this.” I was perplexed. “Why ‘can’t’ you?” I asked. “Because you are proposing we only trade four days a year. What would we do on all of the other days?” The conversation got a bit messy from there. Finally, I asked for clarification. “Just to be clear: You’re saying that when offered the chance to make more money with less work, you are not interested. Is that correct?” I recall a bit of squirming as people wrestled with how that sounded, but the consensus was clear. They were committed to a world of daily uncertainty even if a life of making fewer good decisions was more profitable.

These were people who knew it was difficult to beat the market and understood that one could really only do so by being disciplined and unconventional. But the itch to act, to capitalize on new epiphanies and hunches, to have something to say in an investment meeting, to frequently demonstrate—to themselves, to colleagues, to clients—how smart/worthy/diligent they were was just too great to accept a simple strategy.

The new “new thing”

When I first started learning about climate change and then began thinking about how it would affect the world, I felt the tingle of new greediness. Yes, I cared, but as far as I knew, no one had ever made an investment case based on changing climate conditions. For a short period of time after announcing my investment recommendations, there was a buzz as colleagues and clients searched for ways to exploit the new insights I offered. Chief investment officers of state and national pension funds, big insurance companies, and foundations asked for meetings and presentations.

Some of the big funds made policy changes on the basis of my work, but the faucet of new ideas, arguments, and opportunities to possibly make money by changing your mind stayed open, and every day the five new Morning Meeting pitches were joined by dozens and dozens of emails, each of which had the implicit subject line: “You should change your mind again.” But I didn’t have a new message, not because I couldn’t come up with one, but because I really cared about the risks posed by a changing climate. People knew that I was thinking about climate change all the time, so they would often ask, “What’s new in climate change?” I could tell them that CO2 and CH4 levels were still rising, climate models remained accurate, and the resulting risks were growing more serious, but they had heard that once, and their greed had been sated. Announcing the same thing in the Morning Meeting over and over again wasn’t going to make a dent. So, at the end of 2017, I left the firm and went out to see if I could convince others to be curious about climate change.

My timing was good. Other people and institutions were becoming climate curious. I was happy to give them my time and my ideas. In each case, I told them that they had the opportunity to be leaders but the problem of climate change would require commitment and fortitude. After making a grand announcement about their take on climate change in the global equivalent of the Morning Meeting, each of the new climate leaders was celebrated.

What happened next was familiar: After being praised—at Davos, in the press, by their employees—for pointing out that climate change imperiled the future and would require serious, enduring attention, many of these folks couldn’t stick with the same, steady message. Some gradually went quiet. Others felt the compulsion to promote other “this will change everything” ideas (AI!). Most perplexingly, many began insisting that the problem of climate change had gone from existential to basically solved in a couple of years. They celebrated “breakthroughs” and told us that the inevitable logic of exponential growth was going to kick in for clean energy the way that it had for the other things that had buoyed their fortunes from PCs to cell phones to exchange-traded funds. Policies were in place, solar panels were cheap, and soon there would be green steel and small nuclear reactors in every neighborhood.

Even some scientists were similarly tempted to declare that climate stability was in the newly foreseeable future. They took the scary scenarios off the table, saying it was irresponsible to talk about them. They deemed it recklessly pessimistic to suggest that emissions could continue on a “business as usual” pathway, even though we were still very much on that path. Social scientists and economic modelers drew smooth, S-curve forecasts of the carbon-free future. The climate press, and especially the climate business press (which was also popular for a couple of years), was excited to have a new message, so the scientists claiming that society had “bent the curve” were quoted everywhere. Sure, emissions were still going up, but they were about to go down quickly. It was 2022, the market had caught on, and things were under control.

This dramatic shift was exciting, but assuming that businesses—and societies—will stay committed to an idea, no matter how much initial excitement they had about it, is reckless. We are biologically attuned to incremental information, so shiny new ideas are always distracting, especially if they might offer us a reason to look away from the hard stuff we know we should be doing. It was as if people had seen the “Grand Opening” sign at the newly constructed local gym, had bought fitness trackers, and were now confident that everyone in their neighborhood would soon be fit, strong, and sexy.

Can you handle the truth?

From 2024 to the time of publishing this essay in 2026, private conversations about climate change became bizarre and public behavior became discouraging. CEOs changed their tunes, philanthropists “pivoted,” companies withdrew from climate commitments or simply stopped talking about it at all, and new memes filled all of the available bandwidth. The political winds had shifted and the breeze revealed which people with power were leaders and which were influencers.

In October 2025, Bill Gates released a highly publicized memo about climate change. In it, he claimed that—largely thanks to his Breakthrough Energy fund—we basically have all the tools we need to solve climate change. His detailed list of technologies is reasonable and clear, but it’s like getting a tour of that new gym. Just because it has Stairmasters and Pelotons and climbing walls doesn’t mean everyone will buy a membership and then work out every day or that new gyms are about to be built everywhere in the world. But he has seen enough progress from his vantage point to move on from climate change and thinks others should too. He announced that he was backing away both from climate philanthropy and from climate investing just a few years after having discovered climate change for himself.

I want to take you through Gates’s memo, both to illuminate the problems that climate change poses and because the memo is symptomatic of the kind of communication that is now common.

At the top is the standard meme setup: “A new way to look at the problem.” And then we get the classic rule of three: “Three tough truths about climate.” We have been primed: “Everyone else is wrong about climate; it’s going to be tough to hear this; but I bear the responsibility of telling the new truths that everyone needs to hear.”

“Truth #1: Climate is a serious problem, but it will not be the end of civilization.”

It’s sad that so many of us have been pushed to google the word “truth” lately, but this isn’t even close to being a single truth. There are two statements here, both of which are opinions. The first is supported by evidence, while the second is wild speculation. But what’s most important here is the non-specific language Gates employs. What does “serious” mean? Serious to whom? What does “the end of civilization” mean? He doesn’t say.

“Truth #2: Temperature is not the best way to measure our progress on climate.”

This section of the letter is a classic “say one thing in the first sentence and another in the second sentence and then leave the reader feeling smart and confused at the end” bit. Gates asserts that statistical measures of current human welfare are more important than temperature. That is an opinion. I understand it and can respect it, but it is not a “truth.” It is also objectively not a measure of “progress on climate,” and no other such measures are offered.

“Truth #3: Health and prosperity are the best defense against climate change.”

Here Gates employs another classic influencer trope: Take something reasonable (walking, consuming olive oil, etc.) and make grand claims about it that distract from the stubbornly difficult choices we face. Gates cites an assumptions-riddled thought experiment by a set of American researchers that projects that deaths from climate disasters in low-income countries will fall because people in those countries will be richer and in the past richer people died less often from weather. Gates eagerly builds on top of these assumptions saying, “it follows that faster and more expansive growth will reduce deaths by even more.” In other words, poor people will be able to defeat climate change with money.

When Gates says “defense against climate change,” he seems to mean dealing with a changed climate. This is typically called climate adaptation, and it’s vital, but it is also novel. We can’t look to the past to project the future. To adapt well, people need to understand the specific changes they are going to face. Here, Gates deploys flimsy science-y language to make us feel smart:

We’ll see what you might call latitude creep: In North America, for instance, Iowa will start to feel more like Texas. Texas will start to feel more like northern Mexico.

“Latitude creep” sounds both intuitive and reassuring. The poles receive the least sunlight and the tropics receive the most. A warming atmosphere might have the effect of “moving” every place closer to the equator. Perhaps hearing this little geographic, climatic hack gives you a little burst of dopamine. It feels right, clever, and reassuring: Iowa is at a higher latitude than Texas and both are somewhere in the middle of the US, and Texas is also kind of north of Mexico. Unfortunately, like many such simple grand narratives, it is undermined by reality.

How would it feel?

I happen to know a lot about Iowa, both because I spent a good deal of time visiting my in-laws there and because Iowa had the perfect climate for growing grain. Not only was the range of temperatures great for soybeans and corn, but the specific timing and intensity of rainfall over the state were perfect (spring thaws and showers, heavier rains in June, and then dry and sunny through the harvest), which is why the state became a massive, factory-like industrial complex. We detail Iowa’s climate in the tour of precipitation on the Probable Futures website. I strongly recommend you read it.

I was recently conducting a workshop with a global consulting firm. During a break, an agricultural specialist came up to discuss the distress that Iowan farmers are facing because the water schedule has become unreliable. In recent years, they have faced long dry spells, intense flooding events, and big storms both earlier and later in the year. The consultant is trying to find ways to help farmers who are being forced to constantly invest in new, more advanced, more expensive technology and buy more specialized seeds to defend themselves against the weather. They are doing this with fewer safeguards because reinsurers have abandoned the US Midwest.

Meanwhile, Texas has a whole different set of issues.

The eastern half of Texas is north of the rapidly warming Gulf of Mexico and in the path of hot, humid air and tropical storms. So people in Houston are likely to experience both much larger, wetter tropical storms and summer heat and humidity similar to what residents of Kolkata (which is north of the very warm Bay of Bengal) used to endure.

The western half of Texas is north of Mexico and the rest of Central America. That entire region is becoming radically more drought-prone, and drought has historically been a reliable predictor of migration, which means that Texas—which itself will be more drought-prone—will likely be at the center of ever more intense migration pressures.

And the entire state sits at the southern end of the longest stretch of flat plains south of the Arctic, which is relevant because, as the polar vortex weakens, Arctic air is increasingly likely to wander down into Texas (this has happened twice in the past few years).

I guess Gates could have said that Texas will feel like a mix of the desert, the tropics, and Minneapolis. What about other parts of the world?

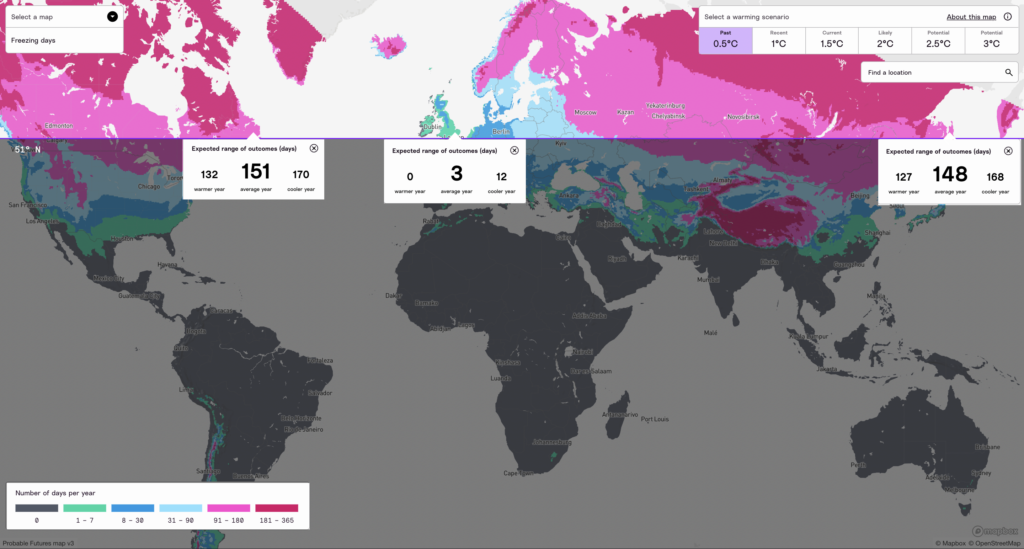

Below is a map from the free, publicly available Probable Futures mapping tool that my colleague Alison Smart and I showed to the leaders of a giant private investment firm in mid-January. It shows the number of days below freezing per year for the late 20th century, when the average atmospheric temperature was 0.5°C above the preindustrial average—a good proxy for the past climate. The meeting was in London, so we highlighted three locations on the 51st parallel. As you can see, coastal places in North America and Asia at this latitude averaged about 150 days per year below freezing, while London had only 3 in an average year, 12 in a cooler year, and none in a warmer year.

On the day we went to their offices, the sun rose at 8:03a.m. and set just eight hours later, and during the so-called daylight hours, the weather was as you picture it: gray and damp. This mildness may be boring, but it was ideal for industrialization and urbanization. This specific climate was key to Western Europe’s industrial and economic success (and the success of the investment firm). What accounted for this exceptional status? The Atlantic Overturning Meridional Circulation (AMOC).

AMOC is an ocean current that has pumped warm surface water from the equatorial part of the Atlantic northwest to the Caribbean, Florida, and the Gulf of Mexico, along the US’s southeastern coast, and across the Atlantic to Western Europe, where its heat flowed onto Britain and the continent, making the winters there mild.

The fact that AMOC could slow or stall has been known by scientists for decades. But now there are not only increasing indications that it has already slowed in recent years but also a clear story for why it might collapse relatively soon. Historically, once AMOC’s warm, salty water (made more saline by evaporation along the way) passed by Britain and Scandinavia, it got very cold. This cold, salty, dense water would then fall to the bottom of the ocean, creating a pull that drove the entire system. But because atmospheric temperatures have risen, especially in the Arctic, Greenland’s ice sheets are melting at a rapid pace, sending vast amounts of meltwater into the ocean. This fresh water is less dense than AMOC’s saltwater and is interrupting the flow of the conveyor belt and could break it altogether.

Here is a summary of a recent research paper in IOPscience:

Under a scenario where Earth warms 2°C over preindustrial levels, the researchers found the AMOC coming to a near standstill, along with dramatically dropping temperatures in Europe during the winter months.

They found, for example, that Edinburgh could see temperatures as low as -30°C. And London, they found, could undergo temperatures as low as -19°C and over two weeks’ worth of days with below-zero temperatures. In the simulation, Oslo was projected to experience below-zero days for nearly half the year. The researchers also found that Scandinavia would grow colder, with some parts enduring temperatures as low as -50°C.

The researchers also note that temperatures in the summer would not change much because temperatures over the continent during the warm months are not impacted by ocean temperatures. That means that the contrast between summer and winter would be extreme. Additionally, other models have suggested Europe would have less precipitation if the AMOC were to collapse, along with a speed-up in sea-level rise.

Western Europe’s natural systems, seasonal patterns, foods, traditions, architecture, energy grid, and water systems would all be screwed up. No infrastructure, ecosystem, culture, government, or company (i.e., the stuff that civilization is made of) in Western Europe is prepared for that. Maybe Europeans would have enough resources to rebuild under these conditions, but it would be hugely expensive and definitely isn’t in any investor’s financial models. And in the tropics, where incomes and wealth are much lower, billions of people rely on seasonal precipitation patterns that were governed by AMOC. How would they adapt to broken monsoons?

“It won’t be cheap”

Gates employs some people I admire and who I know are working hard, so I am sure he got sound advice, but his conclusions are his own, and this is what he says:

Although there will be climate migration, most people in countries near the equator won’t be able to relocate—they will experience more heat waves, stronger storms, and bigger fires. Some outdoor work will need to pause during the hottest hours of the day, and governments will have to invest in cooling centers and better early warning systems for extreme heat and weather events.

Nearly half of all people live in the tropics. How does “latitude creep” affect people who live near the equator? The truth is that people in much of Pakistan, India, Bangladesh, Ghana, Sierra Leone, Chad, Nigeria, Ivory Coast, Columbia, Mexico, Vietnam, Indonesia, Southern China, and many other populous places near warm bodies of water are likely to face life-threatening levels of heat and humidity that no human has ever before encountered. “Although there will be climate migration, most people near the equator won’t be able to relocate” seems like a warning that some societies are in deep danger. But Gates has confidence:

Every time governments rebuild, whether it’s homes in Los Angeles or highways in Delhi, they’ll have to build smarter: fire-resistant materials, rooftop sprinklers, better land management to keep flames from spreading, and infrastructure designed to withstand harsh winds and heavy rainfall. It won’t be cheap, but it will be possible in most cases.

“Every time governments rebuild” is a red flag. “In most cases” is another. Gates started his memo by declaring that climate change “will not be the end of civilization,” implying that “civilization” is a singular entity. But he is acknowledging that people will move, that housing and highways will be destroyed in a warmer world, and that not everyone will be able to rebuild or recover. Many will want to move, but only some will be able to. He is subtly conceding that climate change will cause the end of some civilizations, both because some places will have to be abandoned and because everywhere people will be forced to live in a different relationship to the land, the seas, the living things around them, and the air they breath and rely upon to cool their mammalian bodies.

Gates ends his memo with perfect CEO influencer hype:

This moment reminds me of another time when I called for a new direction.

Thirty years ago, when I was running Microsoft, I wrote a long memo to employees about a major strategic pivot we had to make: embracing the internet in every product we made.

“Got the internet right” will not feature in Bill Gates’s obituaries, even as it pertains to Microsoft. The company did take advantage of its monopoly position in desktop software to make the Internet Explorer web browser (which was inferior to Netscape and Firefox) a binding default. This helped put competitors out of business, which constituted a victory (and eventually led to Microsoft paying large fines for anticompetitive policies). But the list of things that neither Gates nor Microsoft anticipated or successfully capitalized on included search, social media, music, mobile, or, simply the way the internet changed every civilization and our own brains. (Eventually, under the current CEO, Satya Nadella, Microsoft found a boring but profitable internet strategy.)

Gates’s internet memo was about corporate strategy and products, but the climate memo he launched out onto the web is full of grand statements about the future of civilization. He asserts that just as Iowa will feel like Texas, considering what climate change will mean for all the people of the world reminds him of when he thought about what the internet would mean for his company.

The lens of the company is a terrible way to understand society or nature. “Some outdoor work will need to pause” is a peculiar way to say, “It will be too hot to be outside for humans.” “Advances in crop breeding are another great buy” is a peculiar way to say, “The foods people used to eat are not going to make it, so lots of farmers are going to have to buy new seeds from companies, and the people who own those companies will profit.”

Truths and tipping points

Since leaving finance, I have been sharing two big truths that were discovered decades ago by other people:

Truth #1: If we burn vast amounts of coal and oil and transform the surface of the earth by cutting down forests to make pasture land, we will change the atmosphere enough to substantially alter the stable weather patterns we built civilization on. (The International Energy Agency estimates that in 2025 humans burned over 105 million barrels of oil and 24 million tons of coal per day, both record highs.)

Truth #2: A rapidly warming climate is likely to lead to human suffering and societal disruption ranging from minor to catastrophic (e.g., some areas will be too hot for the human body, flooding will render some land unsuitable for agriculture or settlement, drought will induce mass crop failure, violence, conflict, migration, etc.) and not only suffering but extinction for a huge number of other species.

Those two truths felt like enough. But in the past few years, climate science has advanced, partly because modeling has improved but mostly because, as the atmosphere has warmed, scientists have more data from outside the mild, stable past. With each passing year, it is becoming increasingly clear that there is a third truth.

Truth #3: Climate change could cause the end of civilization.

I understand why almost everyone else cares more about other things than they do about climate change. I am glad for that diversity of values and passions. But I am confident that whatever you find valuable, precious, and sacred about life on this planet is likely contingent on a mild, stable climate.

The Amazon rainforest absorbed carbon. Immense stores of carbon stayed locked in permafrost (so named because we assumed the frost was permanent). Glaciers atop Greenland, Antarctica, and elsewhere held mountains of ice and reflected sunlight. And ocean and air circulation patterns moved heat in intricate but consistent patterns around the globe. Scientists knew that these and other dynamics that held our climate stable could cross thresholds beyond which they would stop working for us and begin working against us: The Amazon could be a source of carbon instead of a sink; coral reefs could die off; permafrost could thaw; glaciers could melt; and jet streams could weaken. Warming that we started by burning fossil fuels could get out of control and put us on what is known as a Hothouse Earth trajectory that would cause warming to keep rising even if human emissions were zero or negative.

Gates’s memo implies throughout that—like agriculture, outdoor work, and everything else—the climate system is under human control. It’s a tidy story. The truth, however, is that no one knows for sure exactly how unstable Earth’s systems are. The end of civilization is not a forecast. But it is a real risk. It’s not clear how much AMOC has already slowed, how it might behave as it slows (will it become erratic?), or at what global temperature it would collapse. We don’t know how close we are to being on a Hothouse Earth trajectory. But it is clear that we are at 1.5°C; the consensus among climate scientists is that 2027 is likely to be around 1.7°C; and there is some probability of AMOC collapse and other destabilizing dynamics at these levels of warming. The simple truth is that the future is growing increasingly unstable and risky. Why offer false reassurance?

Fables and temptation

When I first read Gates’s memo (and other recent pronouncements by other corporate influencers), I was angry. But I have learned to try to see the world from other people’s perspectives. I imagined him sitting in his home compound (which he named Xanadu 2.0) feeling the pressure to have a big message, to be the oracle. It’s not an elected role. No one asked him to do it. But he clearly feels the push. In finance, that kind of push loses money. You don’t want to be in a position to have to do something. The best investors avoid those situations, usually by identifying and avoiding risks they can’t estimate or hedge. In contrast, the ones who most reliably lose their clients’ money are the ones who think they are always the smartest people, always have the best ideas, and always feel pressure to act. Indeed, this is what retail investors and bad portfolio managers have tended to do, burning cash chasing the next new thing or the latest emotion. Mathematically, outperforming investors make their money off the people who feel compelled to do something and feel smart.

Noisy financial markets can put this kind of pressure on people, but technology and culture can as well. In recent years, lots of people have signed up for this kind of role. I know they are all over social media and YouTube, but I first noticed them as an early listener to podcasts. About 15 years ago, science-y podcasts popped up to explain everything (The Freakonomics Podcast even called itself “The hidden side of everything”).

Initially, I found these podcasts enchanting, especially Radiolab. Every week the hosts found a new story that made the world seem more amazing. But I began to wonder: How are they going to keep this up? How can there be another breakthrough and grand theory every week? Sometimes the podcasters did their own research, interviewing scientists and experts in detail, and years later those episodes still stand out as excellent. But often they would outsource the gee whiz to prolific writers whose books claimed to illuminate the workings of the human mind. Oliver Sacks and Jonah Lehrer were among the most reliable such guests.

Both Lehrer and Sacks accepted the role of big, exciting, fun ideas guys. Unfortunately, once you commit to a multibook publishing deal, a weekly podcast, or a regular blog, you might get desperate, even greedy, for the new, and your standards for truth might weaken. Before long, both Lehrer and Sacks started making things up. Lehrer was caught after fabricating a story about Bob Dylan for his wonderfully titled book Imagine: How Creativity Works. Sacks’s private writing revealed his regrettable behavior only after his death. In a moving piece in Nautilus, the neurologist Pria Anand reckons with the recent revelations in a New Yorker article by Rachel Aviv that Sacks was a fabulist.

What emerges from Aviv’s deeply reported work is not conscious deception, but the gravitational pull of confabulation, a tidy narrative mistaken for truth. Aviv quotes a letter Sacks wrote to his brother, Marcus, enclosed with a copy of The Man Who Mistook His Wife for a Hat. In the letter, Sacks calls the book a collection of “fairy tales,” explaining “these odd Narratives—half-report, half-imagined, half-science, half-fable, but with a fidelity of their own—are what I do, basically, to keep MY demons of boredom and loneliness and despair away.” In fact, Sacks writes, Marcus would likely call them “confabulations.”

Anand still admires Sacks and finds much of his writing wonderful (I agree, including his writing about music). At the end she says:

But Aviv’s article also left me with an unsettling revelation that transcends Sacks’s writing: not simply that Sacks revised reality, but that we all do. Confabulation is powerful precisely because it slips beneath consciousness, beneath the attention of even the keenest observers. Surrounded by a chaotic world, deluged with sights, sounds, and sensations, our brains instinctively search for narrative order, telling stories to explain away that which we cannot understand and that which we fear. All of us narrate our way through gaps, often mistaking the satisfaction of a tidy story for the truth.

The heat goes on

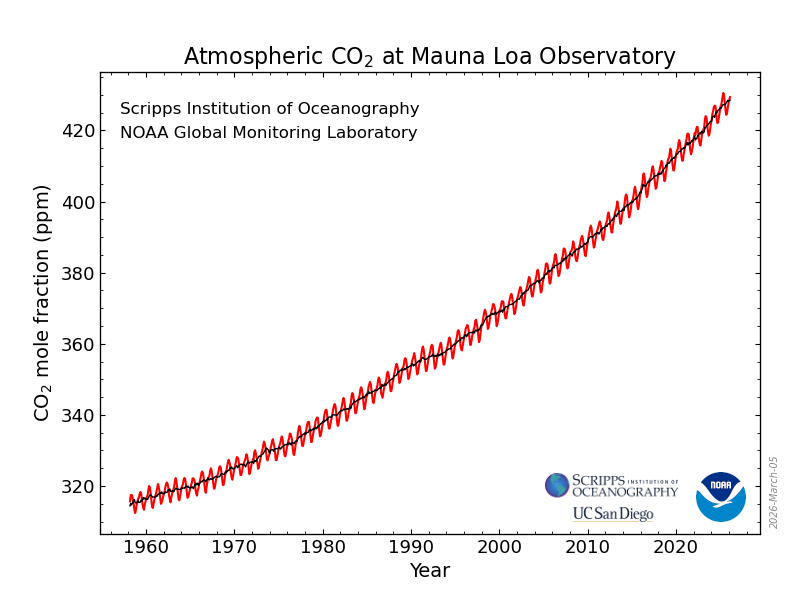

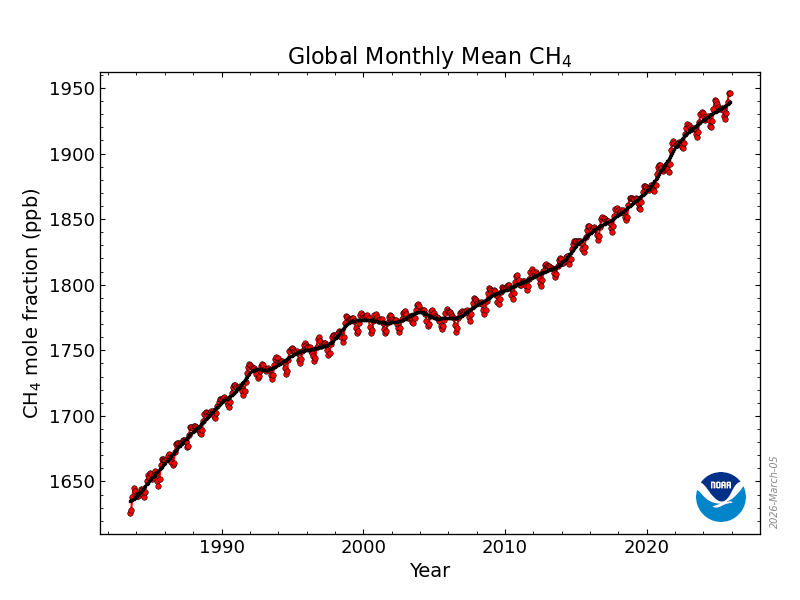

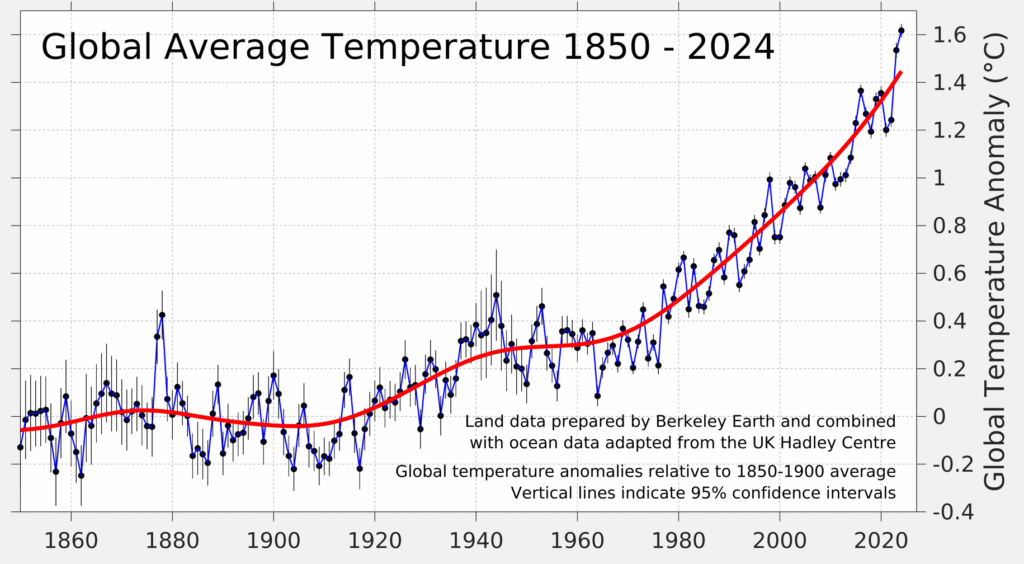

Here are up-to-date graphs of the concentration of CO2 in the atmosphere, the concentration of CH4 (methane) in the atmosphere, and global average temperature:

I wish they weren’t true.

Voting, and weighing

The legendary value investor, Benjamin Graham, said, “In the short run, the market is a voting machine, but in the long run, it is a weighing machine.”

The most successful investors I have known had a sense for when markets were likely to shift from voting (opinions) to weighing (truth). Leading up to the fall of 2008, US housing prices had risen dramatically. Since they had not fallen in almost 100 years, almost every macro model assumed they couldn’t, and the media was full of grand “it will all work out” narratives that encouraged everyday people to take out more debt, buy more houses, flip them, etc. At the firm, there were a couple of analysts and portfolio managers who had patiently met with virtually every bank in America and with the investment bankers behind the boom in securitized mortgages. These folks rarely spoke in the Morning Meeting, so when they declared that many AAA-rated bonds were likely to be worthless, it was noteworthy. I even helped arrange a meeting at the Federal Reserve so that regulators could hear their insights, but the Fed economists were confident that the times ahead would be peaceful.

Attention could come back to climate through markets: The weighing machine could reveal that investors—from big fund managers to individuals who took out a mortgage in Texas or London or borrowed for their crop in Iowa or Kenya—had taken on risks they underestimated. It’s likely. Just in the past few weeks, executives at African banks have told me that they can’t lend any longer to farmers in their community, and private equity investors have announced at conferences that they are moving out of southern Texas (“If you are uninsurable, you are uninvestable”). A Brazilian mining executive told me that if rainfall continues to be erratic and intense, it will be impossible for his company to deal with the toxic tailings that mining produces.

Even more commonly, people in finance tell me that they continue to put money into risky places because their clients tell them to (“We know Florida real estate is a Ponzi scheme, but our clients insist, and it’s their money”). Some of the folks who correctly anticipated the 2008 crash are creating investment funds to catalyze a crisis. That may sound harsh, but it’s a social positive: The sooner people realize that we are all taking dangerous risks, the better.

But waiting for financial markets to tell us that we face tough moral, ethical, and cultural decisions is a bad way to engage with the future. Michael Lewis wrote an excellent book about the global financial crisis called The Big Short (it’s also a terrific movie). If you listen to the characters Lewis interviews, they don’t talk about money, about good or bad buys, or about being clever. They don’t offer life hacks or cognitive tricks. Like my colleagues who saw the 2008 crisis coming, they focus on corruption, bad regulation, and the irresponsibility of public figures, financiers, and corporations who avoided making hard decisions, shifted the risks onto other people, and looked out for themselves.

The future is full of things that are hard to understand and anticipate (every podcast now seems to be an AI guessing game as is, I assume, the Morning Meeting), but you don’t need Bill Gates to tell you what to think about climate. You almost certainly already know enough to understand that addressing climate change will be good for civilization, no matter how you define it. You also have a good sense of what actions you, your community, and your government can take to both limit the risks your community faces and to limit the disruptions, chaos, and suffering that would likely result from higher temperatures, big changes in precipitation, and higher seas. It’s not about being clever or smarter than everyone else—it simply requires adhering to old, well-known disciplines of honesty, generosity, and compromise. You could even reduce it simply to being curious and civic.

If you are unsure or simply want a reminder, my colleagues and I built Probable Futures as a reliable source to help you find your way. It’s like a lighthouse.

Onward,

Spencer